Finding the Next Solana

The Quest for Next-Generation Layer 1 Blockchains

Join industry giants like Coinbase, McKinsey, HBS, Coinbase, JPM and leading VCs for unparalleled independent insights. Subscribe now and stay ahead of the curve.

I. Introduction and Background

Coming out of Breakpoint 2024, Solana seems like it can do no wrong. Since its inception four years ago, there hasn't been such electric hype around the blockchain - not even during SBF's "sell me all your Solana and fuck off" phase. The numbers tell the story: fourth most valuable L1 by market cap, third biggest protocol by TVL, first in active addresses, and a casual 274x price appreciation from launch to peak. Not bad for a chain that was supposedly "dead" after FTX collapsed.

However, questions arise:

Is blockspace just a commodity no matter which blockchain it is on or is there something special about Solana?

Will we ever see another Solana?

There is a nonzero chance we will.

A new generation of Layer 1 blockchains believes they can challenge Solana's position. Sui, backed by ex-Meta blockchain developers, is building for gaming and TradFi applications. Aptos, sharing similar Meta DNA, takes a Web2-friendly approach to enterprise adoption. Sei focuses on high-performance DeFi. Meanwhile, pre-launch chains Monad and Berachain are redefining what a Layer 1 community can look like, combining technical innovation with memetic appeal.

This analysis explores whether any of these contenders can replicate Solana's success or if they're destined to join the graveyard of "Ethereum killers" and "Solana killers" that came before them. By examining their technical innovations, community-building approaches, and early traction metrics, we'll assess their chances of success in an increasingly competitive landscape.

II. Do Modern L1s Perform Better Than Solana?

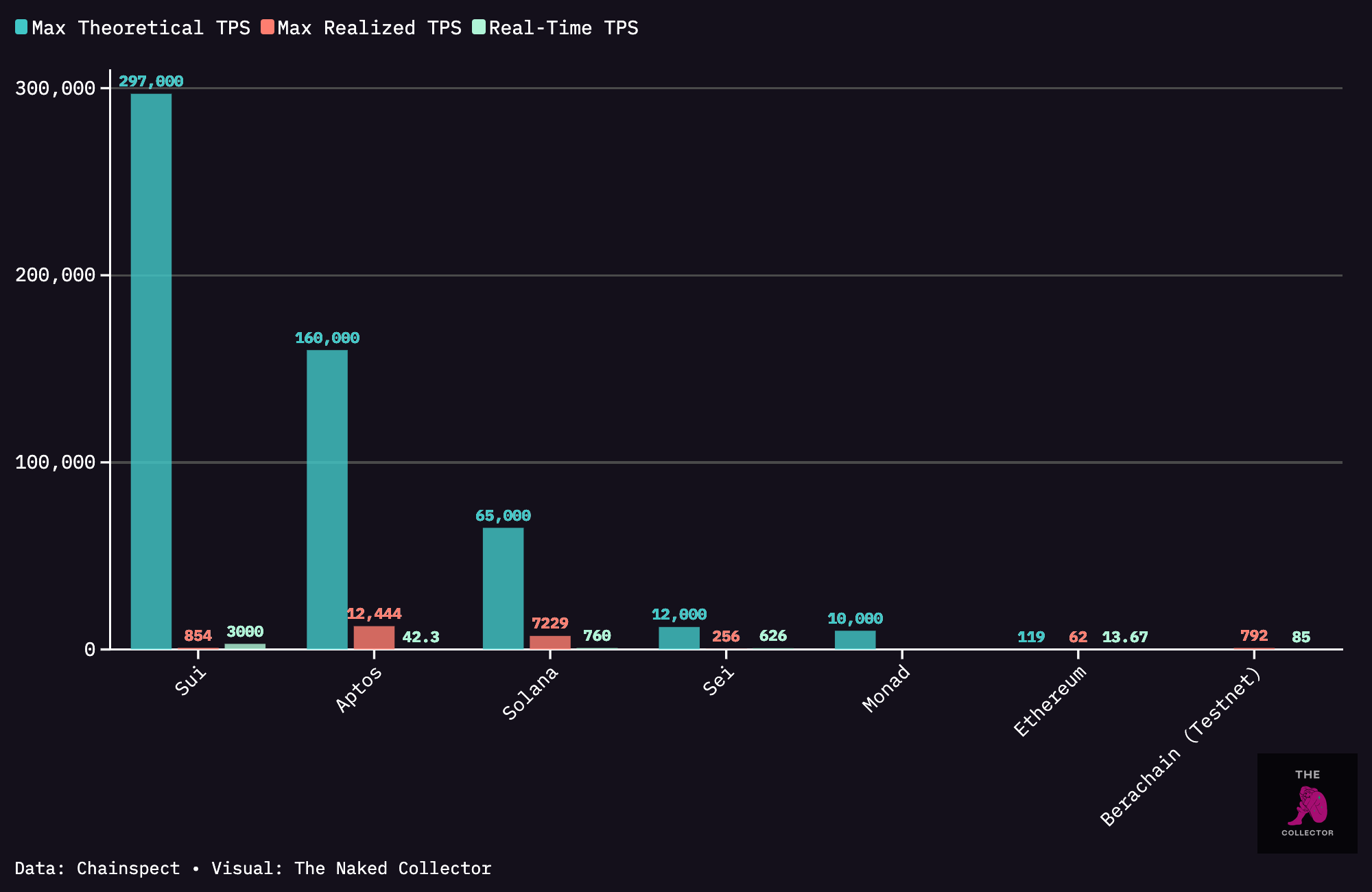

Are They Faster Than Solana?

A new wave of Layer 1 blockchains - Monad, Sei, Aptos, Sui, and Berachain - all claim significant performance advantages. While they offer improvements in speed, composability, and development ease, each takes a distinctly different path to achieve these goals.

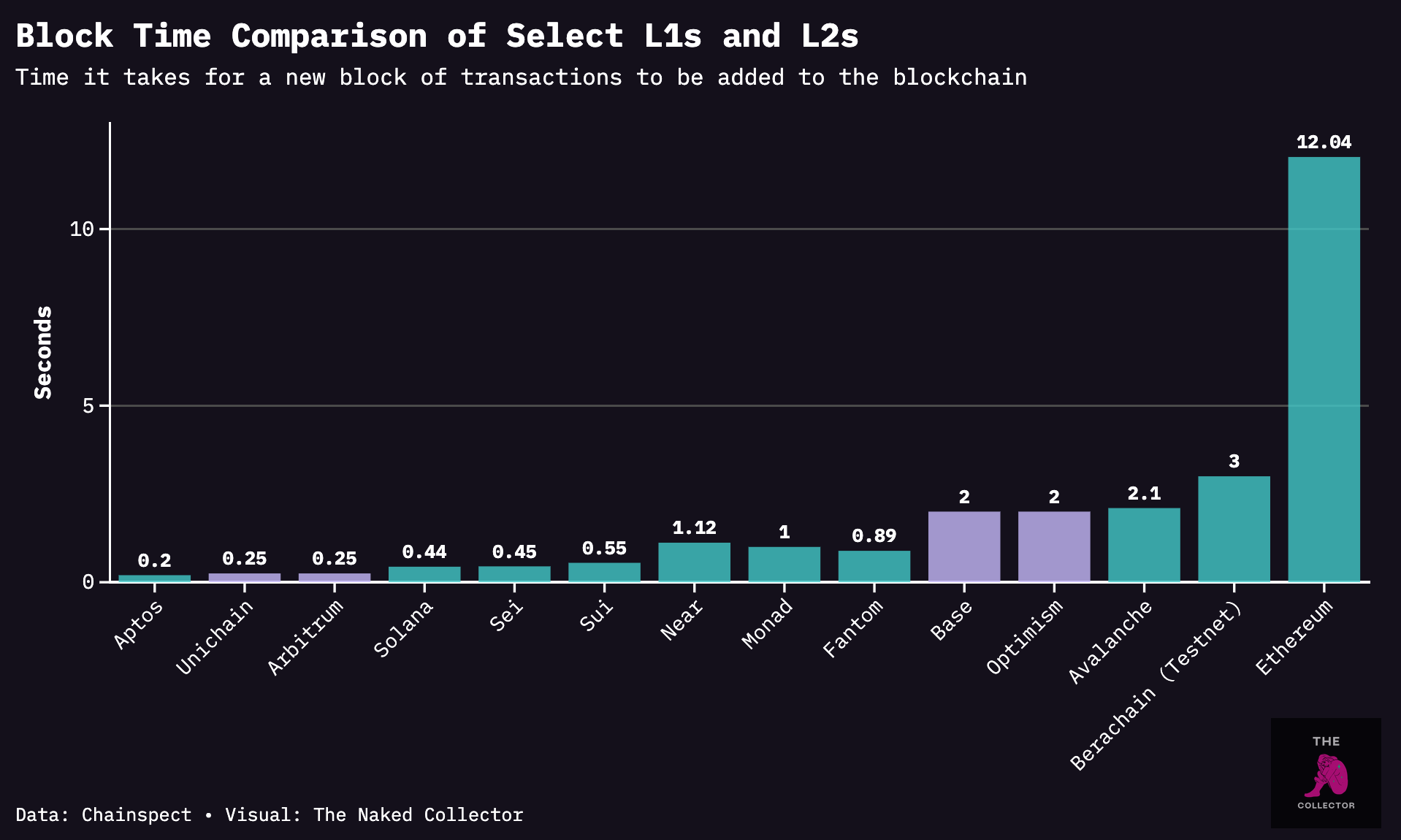

The three major speed categories are transactions per second or TPS (how many individual transfers or operations the network can process each second), block times (how long it takes to create a new block of transactions), and time to finality (how long until transactions become irreversible).

Performance metrics require careful analysis. Though some Layer 2 solutions boast faster block times than these new L1s, their overall time to finality remains constrained by their underlying Layer 1 chain, particularly Ethereum's finality limitations. See charts below:

The most significant advances in these new Layer 1s come from their transaction processing speed and cost structure. Some experts argue that modular blockchains (L2s) fundamentally cannot match the speeds of monolithic chains, though emerging solutions like Unichain, Arbitrum, Fuel, and MegaETH may challenge this assumption.

Whatever the case may be, Layer 1s maintain a crucial advantage: the ability to preserve common state, shared liquidity, and unified user experience - benefits that remain fragmented across Layer 2 solutions.

Are They Cheaper Than Solana?

The unique Layer 1 architecture allows these blockchains to charge substantially lower gas fees than both Ethereum and Solana. While the lower fees may not be a game changer for the average user, they become significant in two scenarios:

Mass adoption - when we reach billions of users

High-frequency trading - where performing thousands of transactions per day makes 10x lower fees critically important

Keep in mind that Solana has been congested recently due to memecoin trading activity, affecting its fee structure.

Another significant advancement in these new alternative Layer 1s is single-slot finality. Both Ethereum and Solana currently use multislot finality (though Ethereum has been looking to shift to single-slot for a while now). Single-slot finality allows transactions to finalize in a second or less, enabling:

Instantaneous on-chain hedging

Complex trading operations

Reduced volatility exposure

In contrast, a multislot environment's longer finality time and potential block reorganization forces users to absorb unnecessary volatility – potentially eating into the profits of market makers and traders alike.

While the lower fees aren’t a game changer for the average user, they could make a difference for on-chain high frequency trading. Having 10x lower fees matters when performing thousands of transactions per day. Another leap forward for these new alternative Layer 1s is single-slot finality. Both Ethereum and Solana use multislot finality (Ethereum has been looking to shift to single-slot for a while now). This allows the transaction to finalize in a second or less.

How Do They Do This?

How are these L1s capable of such speeds and low transaction costs? In short, it’s because they’ve designed their blockchains from first principles.

Remember that blockchain transactions are made up four key elements:

Execution: Processing and validating transactions

Consensus: Achieving agreement among nodes on transaction validity

Data Availability: Ensuring transaction data is accessible

Settlement: Finalizing transactions and resolving disputes

The key innovations emerge primarily in execution and consensus mechanisms. In execution, two distinct approaches have emerged:

State Access Parallel Execution (Sui, Solana)

Requires explicit declaration of state access (transactions have to explicitly declare which parts of the blockchain state they will access before execution)

Enables efficient resource pre-allocation

Increases developer complexity

Optimistic Parallel Execution (Sei, Aptos, Monad)

No pre-declaration requirements

Parallel processing without conflict checks

Simplified developer experience

Source: The Naked Collector

See the chart below for further comparison between state access and optimistic parallel execution methods:

Each chain also implements proprietary consensus mechanisms designed for speed: Sui's Mysticeti, Aptos' AptosBFT, Monad's MonadBFT, and Berachain's Proof-of-Liquidity. These mechanisms streamline block creation while maintaining security. Additionally, custom database implementations (Aptos’ Block-STM, Sui’s Objects Model, Sei’s SeiDB, and Monad’s MonadDB) optimize the data availability layer for improved retrieval speeds.

Why Speed Matters

Generally, for three reasons:

MEV Reduction: Faster finality significantly reduces maximal extractable value opportunities, effectively lowering transaction costs for users.

Enhanced User Experience: Sub-second finality enables true real-time applications:

Gaming: Instantaneous microtransactions

Trading: Precise hedging execution

Interactive Applications: Sub-0.1s latency (approaching Web2's 0.02s standard)

Institutional Appeal: Jump Crypto's investments in Sui, Sei, and Aptos validate the importance of these improvements for institutional adoption.

Performance Context:

Visa: 24,000 TPS

Mastercard: 5,000 TPS

Solana (after Firedancer improvement): 600,000-1,000,000 TPS

While these L1s demonstrate architectural innovation, their performance advantages appear incremental rather than revolutionary. Block times and TPS metrics show comparable performance to Solana, and the upcoming Firedancer validator client may further extend Solana's capabilities.

However, the real opportunity lies in reliability rather than raw speed. Solana's 40% failed transaction rate, primarily from DEX-related slippage and bot activity, presents a clear vector for differentiation. For transaction-intensive applications like high-frequency trading and gaming, consistent execution may prove more valuable than marginal speed improvements.

These new Layer 1s are attempting to address these reliability challenges, provide higher speed and lower fees through their unique approaches to execution, consensus, and data availability.

III. Can Modern L1s Beat Solana?

Technical Foundations: EVM, Development, and Decentralization

As we examine whether modern L1s can challenge Solana, a fundamental question emerges: Does EVM compatibility provide a meaningful advantage? Three of the five new alternative Layer 1s (Sei, Monad and Berachain) believe it does, making EVM compatibility central to their strategy.

EVM compatibility enables seamless redeployment of Ethereum smart contracts onto these new chains. This means Solidity developers can continue using familiar tools like Foundry, Remix, and Hardhat, while users maintain their existing workflow with Metamask (or other wallets) just by changing RPC settings. While the benefits of parallelization are clear, we must examine whether EVM compatibility truly matters given Solana's success without it.

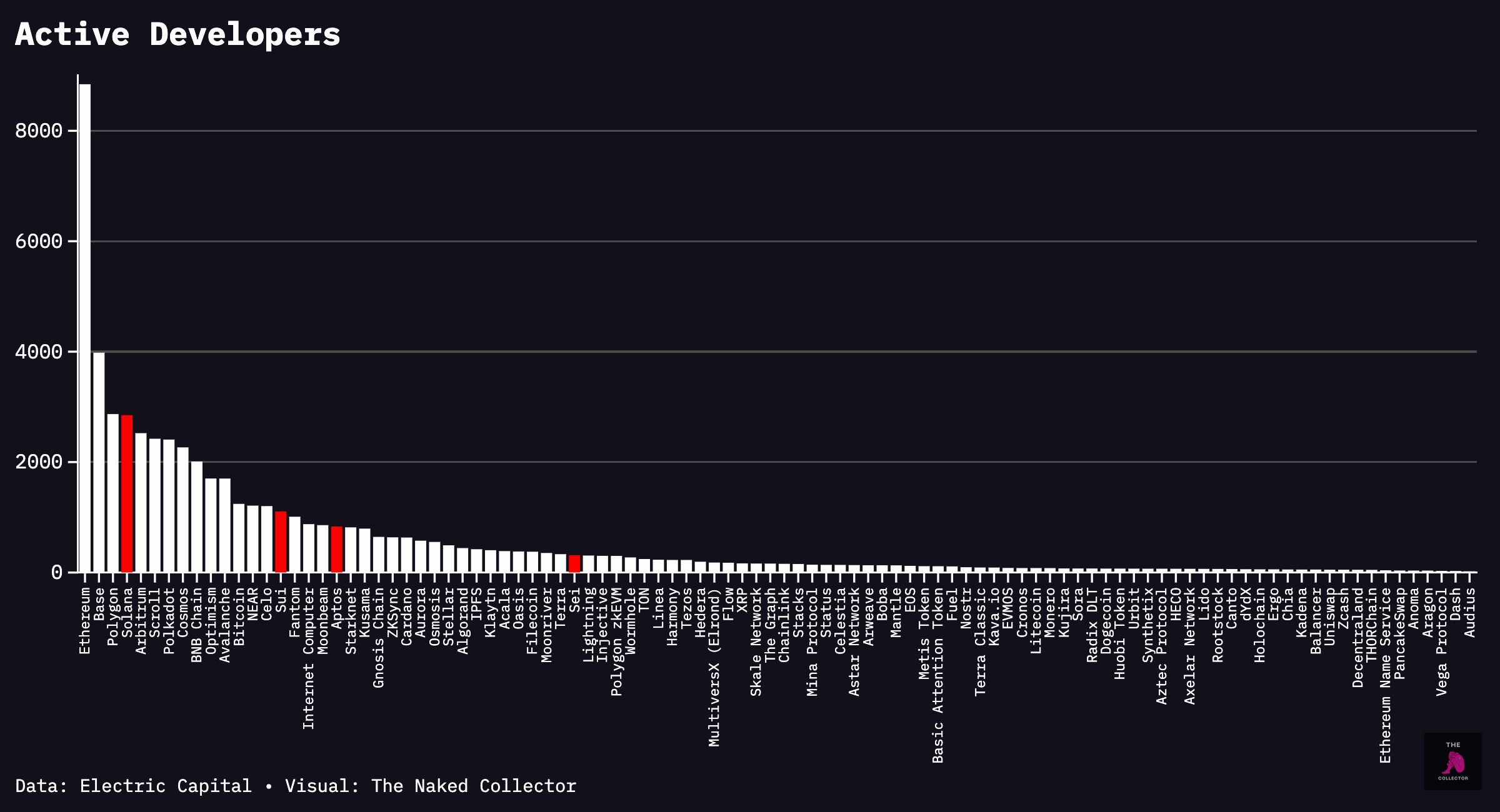

Looking at developer adoption first, Ethereum still has the lead over developer mindshare.

Not only do developers want to build on Ethereum, but it has 3x the developers (part-time + full-time) Solana has.

This advantage manifests even more dramatically in new smart contract deployment, where EVM has tens if not hundreds of thousands of contracts while Solana contracts are in the hundreds.

While the pool of builders is certainly larger for EVM chains, whether these EVM developers will benefit the new compatible L1s remains to be seen. For one thing, both Sui and Aptos (non-EVM blockchains) have 3x developers and higher developer interest than the EVM-compatible Sei has.

Beyond developer metrics, TVL presents a more complex picture. While EVM chains have a clear lead over non-EVM chains (Ethereum alone has over 50% of the TVL at the time of writing), the EVM-compatible chains Aptos, Sei, Sui and Monad won't get a portion of that TVL automatically. Analysis of Ethereum Layer 2s suggests a more modest potential: around 2% TVL unlock for EVM Layer 1s like Berachain and Monad, as these could be perceived as more similar to Ethereum, something some users may value.

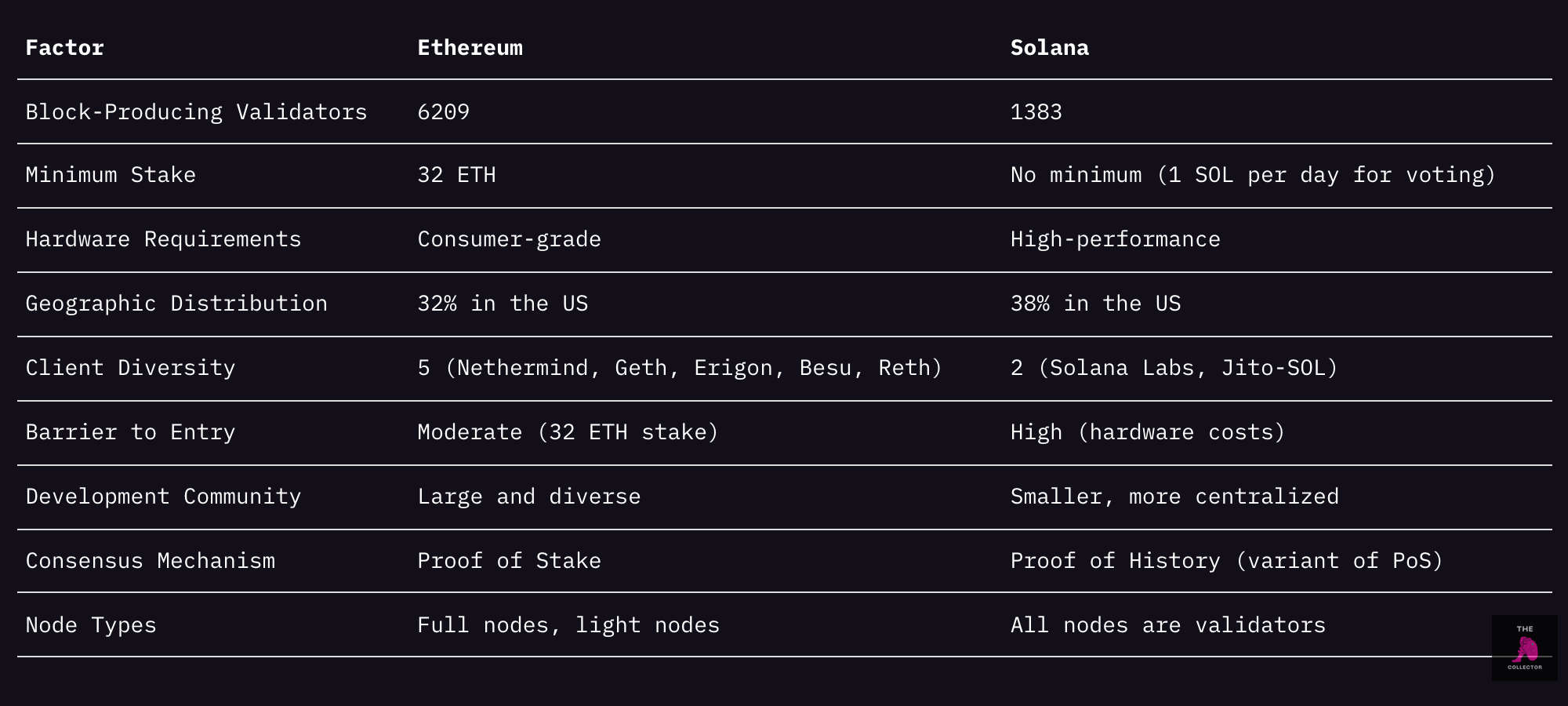

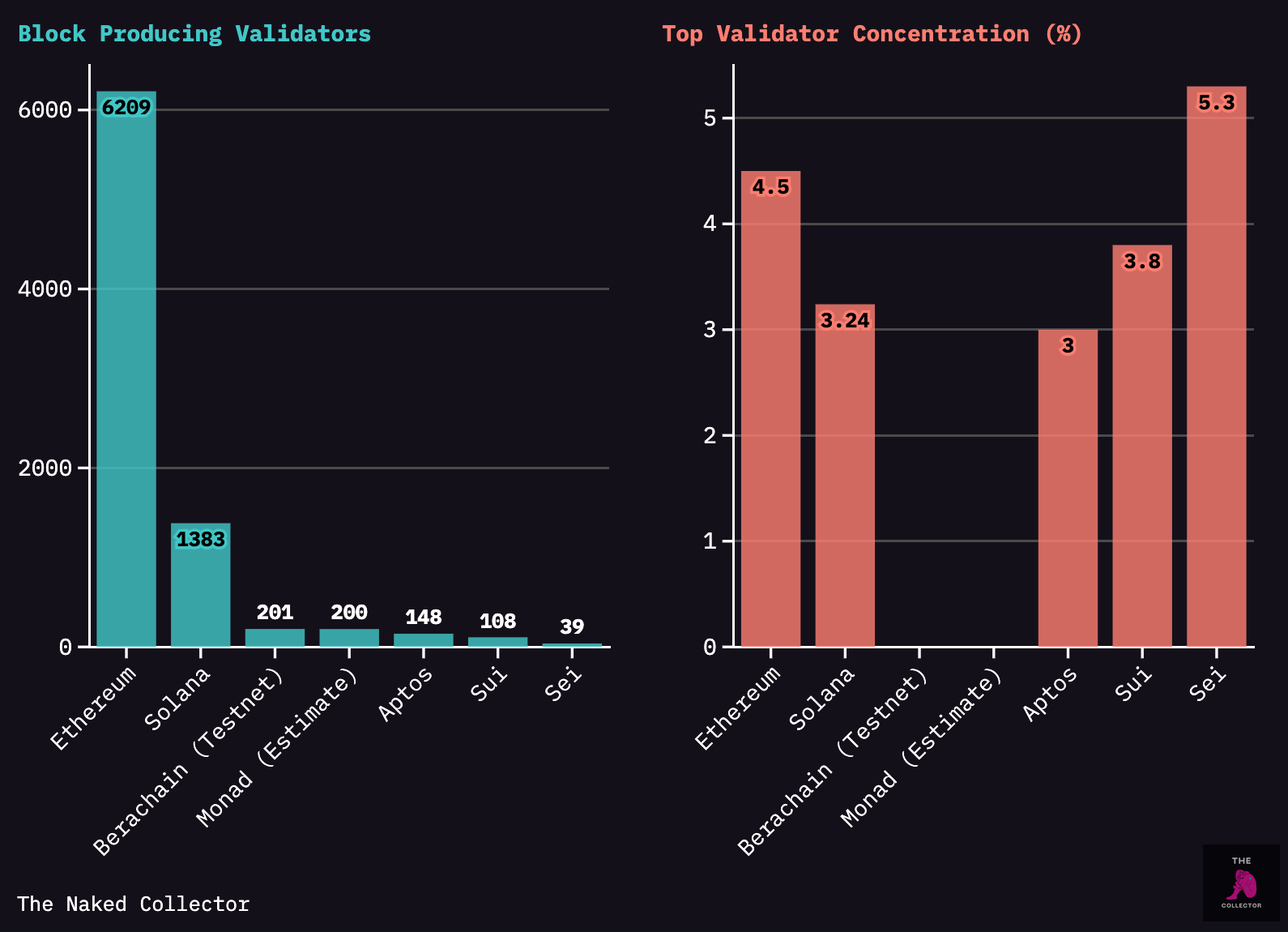

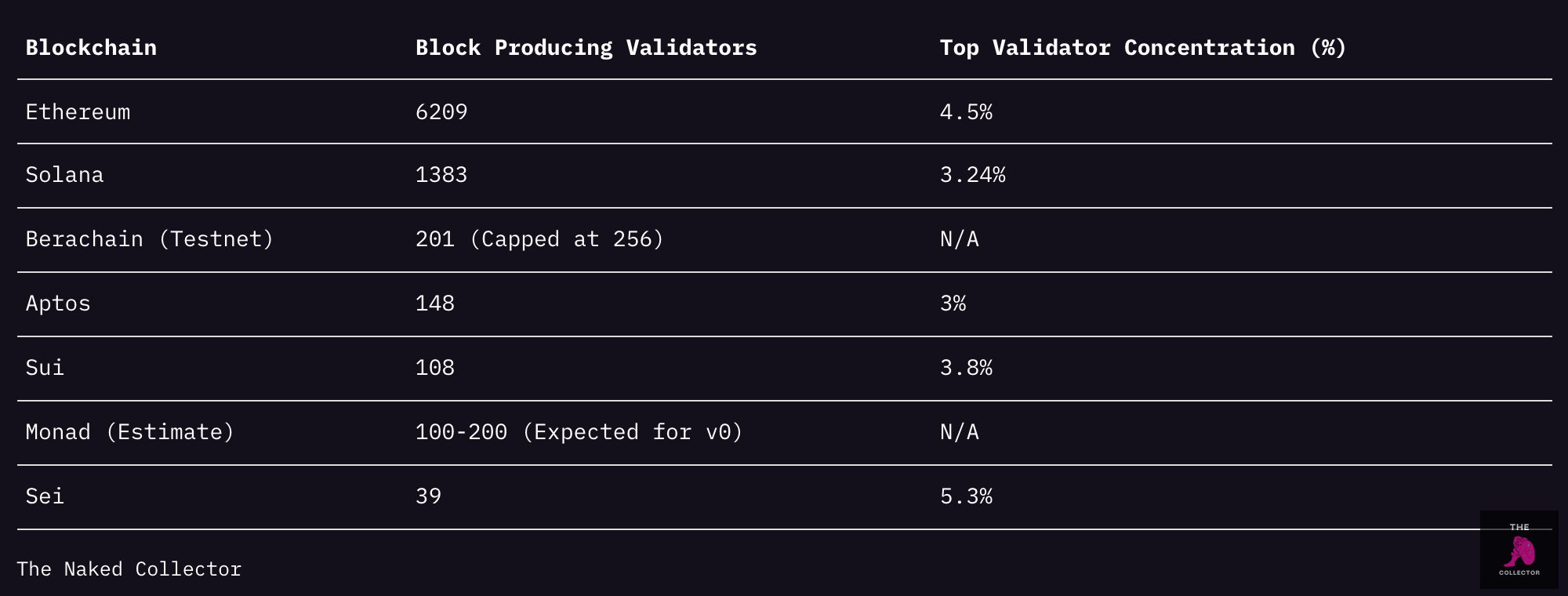

The decentralization question adds another layer of complexity. While lower hardware requirements are often associated with Ethereum and to some extent with the EVM ecosystem, the reality is more nuanced. Ethereum's total validator count far exceeds Solana's, but these validators are concentrated in the Lido protocol. What matters more for decentralization are the block-producing validators.

Solana takes a different approach. While its hardware requirements are higher, its vision emphasizes democratized verification rather than validation, providing transparency over the blockchain. Notably, Solana has no minimum staking requirements, unlike Ethereum's 32 ETH requirement for solo validators.

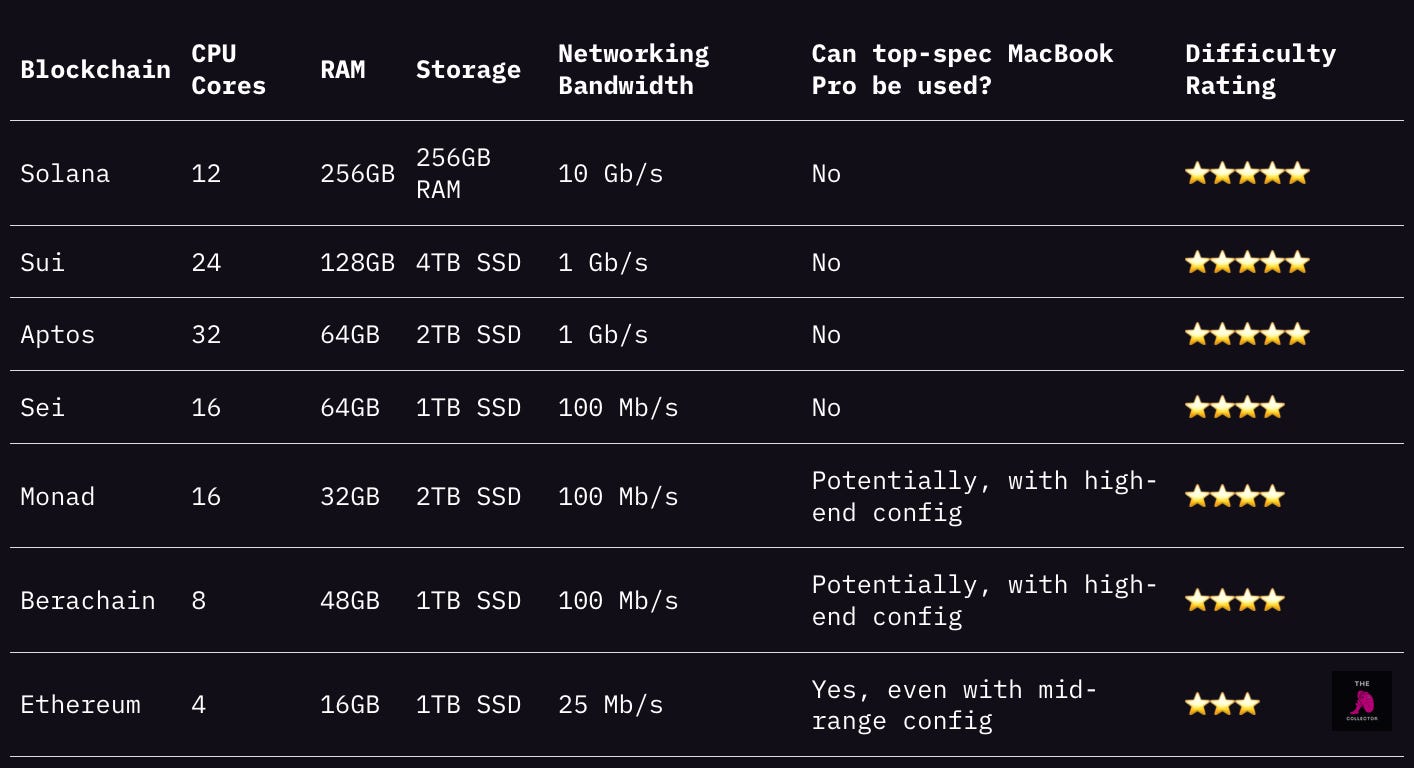

To understand the theoretical potential for decentralization across these new L1s (i.e., can anyone with a high-end MacBook Pro run a validator node), I analyzed the minimum specs for running a node on each blockchain. Solana shows the most prohibitive specs while Ethereum has the least. Perhaps unsurprisingly, the new non-EVM Layer 1s Sui and Aptos align closer to Solana's higher-end hardware requirements.

Yet in practice, we see little correlation between validator count (or decentralization) and EVM compatibility at the time of writing.

The lower validator counts on these new L1s partly reflect their higher hardware requirements. While we must consider their youth and commitment to making blockchain verification (rather than validation) accessible, none can yet claim to surpass Solana in decentralization.

These higher hardware requirements result in lower validator counts across the new L1s. Though they're still young and focus on accessible blockchain verification rather than validation, none currently rival Solana's (much less Ethereum’s) decentralization metrics.

The Case Against EVM Compatibility

Modern cross-chain solutions have transformed the user experience landscape. With DeBridge, LayerZero, and Wormhole offering seamless and cost-effective bridging, the distinction between EVM and non-EVM chains has blurred from a user perspective.

Instead, chains now compete on three key fronts:

Transaction fees: E.g. Aave on Arbitrum is cheaper post-fees than Aave on Ethereum. However, with most new L1s offering similarly low fees, this is quickly becoming a commoditized feature.

Security (including decentralization): Critical for institutions and large stakers. Ethereum currently leads here, benefiting from the Lindy Effect, while these new Layer 1s face initial disadvantages in gaining trust.

User-valued applications: Perhaps most crucially, users follow compelling use cases regardless of chain loyalty. Even the most dedicated Ethereum supporters bridged to Solana for NFTs, just as they now explore Solana's thriving DePIN ecosystem. Use cases trump allegiances.

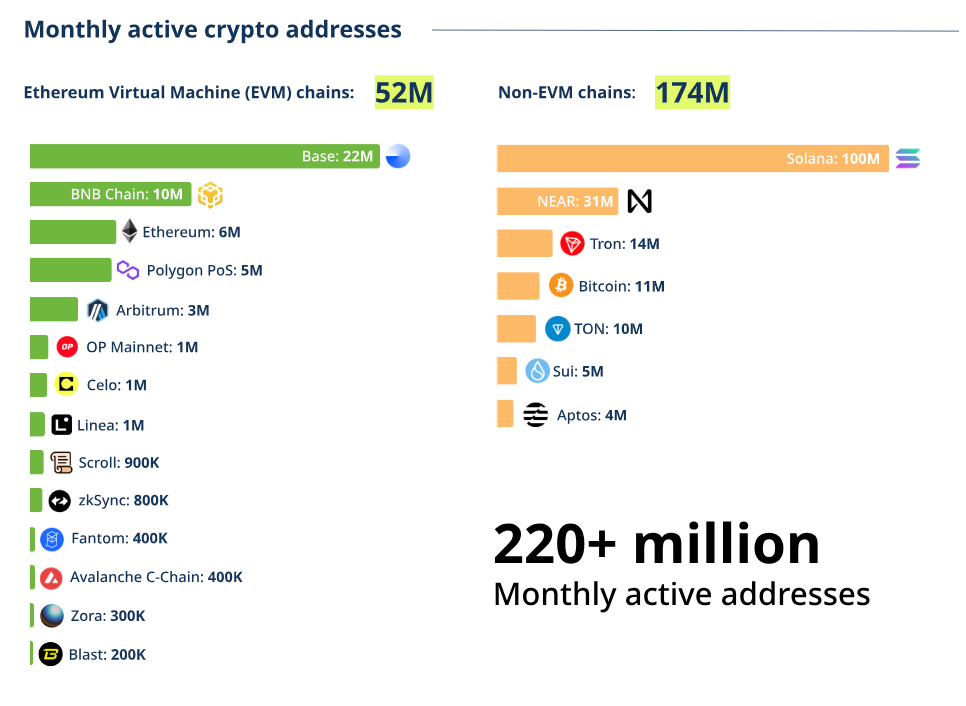

The data reinforces this user-centric view. Non-EVM chains show more than 3x more active wallets according to a16z (though some of this reflects bot activity).

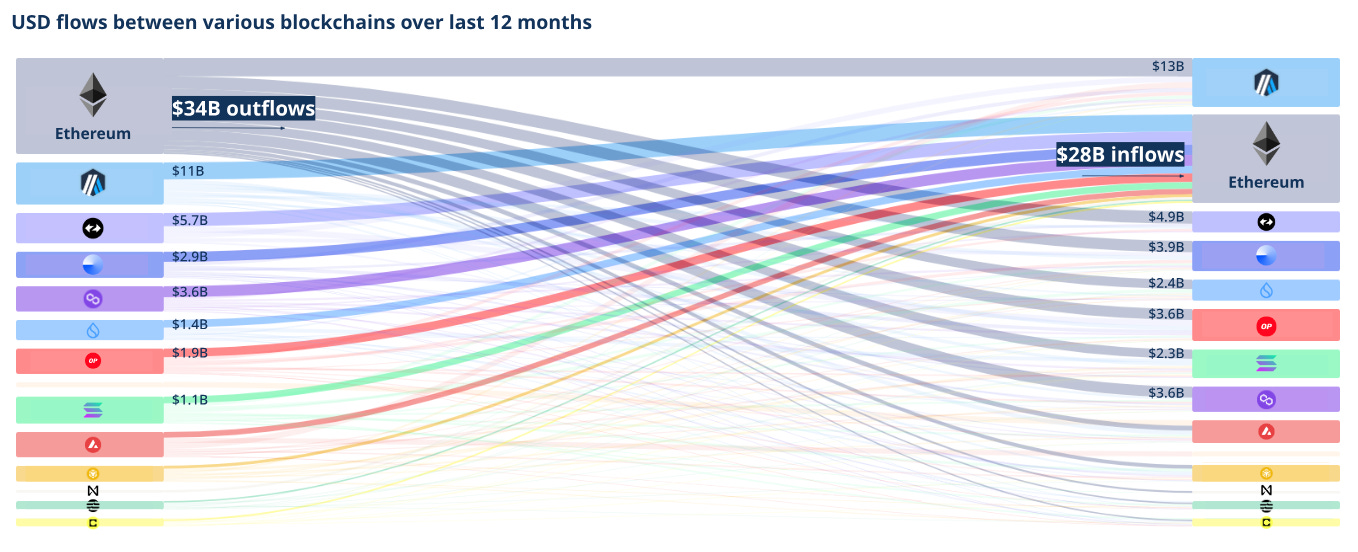

Moreover, Solana's ecosystem shows stronger cross-chain appeal, with more inflows from Ethereum than outflows back to it.

These patterns suggest that EVM compatibility alone doesn't guarantee network effects or liquidity – as evidenced by numerous dead EVM-compatible chains. Some of them seen below.

Base's success illustrates this point: its growth stems more from Coinbase's established user base than from EVM compatibility.

In summary, while EVM compatibility may not completely eliminate user experience friction, Ethereum still captures the majority of developer mindshare and offers significant advantages. The dApps built by these developers can be ported over to EVM-compatible chains, though this doesn't guarantee user adoption. Ethereum also has promising developments in ZK technology, including account abstraction (Safe adoption, ZKEmail, EIP-7702) and ZK-SNARK applications (Zupass, Railway, 0xbow, Rarimo). The analysis shows decentralization depends more on hardware requirements and design choices than EVM compatibility, and TVL doesn't automatically transfer to new EVM chains. Most importantly, user adoption follows compelling applications rather than technical compatibility, explaining why non-EVM chains like Solana can thrive. This suggests new L1s need more than EVM compatibility to compete effectively.

Next, we will look deeper into the competitive advantage of each of these new Layer 1 blockchains.

User-Centric Gaming & TradFi Innovation – Case: Sui

Founded by the ex-Meta blockchain team and launched in May 2023, Sui has emerged as a prominent Layer 1 contender. While Mysten Labs' CEO Evan Cheng positions Sui as a general-purpose blockchain, its architecture reveals a natural advantage in gaming and social applications, driven by three key strengths: seamless user experience, powerful gaming primitives, and TradFi-ready infrastructure.

User Experience & Gaming Features

First, seamless user onboarding removes traditional Web3 friction points. Users can create wallets using Gmail accounts and Face ID, while gasless transactions at the protocol level eliminate the complexity of managing gas fees. This foundation enables mainstream adoption of blockchain gaming.

Second, Sui's technical architecture directly enables new gaming experiences:

Dynamic NFTs evolve with player achievements. For example, in Legends of Arcadia, character NFTs can upgrade based on player decisions and in-game accomplishments

Zero-lag gameplay through efficient transaction processing enables real-time multiplayer interactions

Asset composability (similar to ERC6551) where objects can own other objects

Programmable Transaction Blocks (PTB) handling up to 1,024 operations at once, enabling complex in-game actions like:

Mass crafting of items

Trading entire inventories in one transaction

Executing complex multi-step quests

The Sui Kiosk system powers new economic models:

Players can run their own in-game fashion stores

Artists can create in-game galleries to sell generative art NFTs

Sui primitive also allows NFTs to be sold only if conditions are met. These conditions could dictate that 1) royalties are paid and 2) they are sold only via a specified marketplace.

Sui’s Time Capsule NFT primitive allows NFTs to be revealed at a specific time giving rise to:

Timed weapon or character reveals

Scheduled in-game events

Raffle reveals or in-game betting

Obfuscated NFTs create novel monetization options:

Try-before-you-buy item previews

Progressive content unlocks

Premium feature reveals

These capabilities are further strengthened by robust infrastructure:

SCION (Scalability, Control, and Isolation on Next-Generation Networks) integration providing DDoS protection and improved connectivity

Mysten Labs-built Walrus protocol enhances Sui's scalability by moving away from traditional Web2 storage solutions

SuiPlay0X1, a dedicated gaming console with native support for Sui Web3 games (Solana is responding with its own gaming console Play Solana)

Sui’s Web3 gaming discovery and education website

Company-specific loyalty points using the Closed-Loop Token standard

Sui also emphasizes Web2 company adoption through several key features:

The Closed-Loop Token standard enabling company-specific loyalty points and rewards programs

Enoki, a SaaS platform from Mysten Labs, allowing Web2 companies to seamlessly integrate with Sui for:

In-game asset trading

Loyalty program management (I’ve written about their benefits extensively here)

Custom token implementations

Sui’s Enoki pricing. Source: Enoki

Developer support is also particularly strong:

1:1 engineering office hours with the core team

Move programming language designed to minimize common smart contract vulnerabilities like re-entrancy and arithmetic overflows (in 2023 almost $2B of value was lost due to hacking)

Comprehensive documentation and development resources

Source: Chainalysis

Beyond gaming, Sui targets institutional adoption through two key offerings:

First, its Closed-Loop Token standard (i.e. permissioned tokens and the equivalent of Token Extensions on Solana) supports:

Regulated digital currencies

Corporate tokens and rewards

Restricted investment products

Time-locked compensation

Regulatory sandboxes

Regulatory-compliant trading

Programmable grants or subsidies

Tokenized carbon credits

Second, DeepBook, Sui's central limit order book, brings institutional-grade DeFi capabilities:

High-frequency trading applications leveraging Sui's fast finality

Aggregated liquidity pools supporting large-scale trades

Advanced trading strategies including limit orders and flash loans

Professional trading features that move DeFi closer to traditional finance capabilities

Current Ecosystem Status

Sui’s early ecosystem traction shows promise across multiple sectors. It’s most used dApps by sector are:

Social: RECRD – A Web3 TikTok competitor with 481K daily active addresses

Gaming: Birds – 163K daily active addresses. A Telegram mini app so take it for what it’s worth).

DeFi: NAVI Protocol – $294M TVL – The Aave of Sui, but still only 3% of Aave’s TVL

Sui's 2024 Overflow Hackathon showcased both ecosystem potential and challenges, drawing 352 project submissions from 79 countries. The winning projects across different categories revealed interesting insights about Sui's competitive advantages:

In gaming, where Sui's unique features shine, AresRPG won first place with its procedurally generated MMORPG world – a project that leverages Sui's gaming-specific capabilities.

However, winners in other categories highlighted the platform's current limitations:

Consumer category winner Pandora Finance (a decentralized prediction market for token prices, events, and commodities) has only 2.5K users and doesn't justify Sui's high-performance features. Without millions of concurrent users or an on-chain order book, such platforms could operate effectively on simpler chains like Polygon, as Polymarket has shown.

DeFi winner Hop Aggregator (Swap aggregator meets Pump.fun), while valuable for the ecosystem, largely replicates functionality already available on Solana

The analysis of Sui reveals a clear pattern: while it offers comprehensive Layer 1 capabilities, its true competitive advantage against Solana lies in specific verticals rather than general-purpose functionality. Its gaming-focused features, from dynamic NFTs to sophisticated in-game economies, represent meaningful innovation rather than mere technical iteration. The platform's early traction (with 481K daily active addresses on RECRD and significant gaming engagement) suggests this focused approach can work.

However, Sui's experience also demonstrates a broader truth about competing with Solana: technical capabilities alone aren't enough. While Sui offers impressive features like DeepBook for DeFi and Closed-Loop Tokens for institutions, the hackathon results show that many applications don't yet require such high performance. Success appears to come from identifying and dominating specific verticals (in Sui's case, gaming and Web2 integration) rather than trying to outperform Solana across all dimensions.

As we examine other Layer 1 competitors, this lesson about focused differentiation versus general-purpose competition will prove crucial.

High-Performance DeFi Infrastructure – Case: Sei

Founded by an ex-Robinhood engineer and Goldman Sachs investment banker, Sei launched in August 2023 with an initial focus on DeFi. While now positioning itself as a general-purpose blockchain, its technical architecture reveals its DeFi roots.

Technical Architecture & Features

Sei offers EVM compatibility with a unique twist: while Ethereum and Sei wallets have different public addresses, they share the same private key, enabling cross-chain access.

However, this compatibility still requires users to complete a five-step process, somewhat limiting its practical benefit.

Like other new L1s, Sei offers low gas fees through parallelization. One of Sei's points of differentiation is its proactive approach to MEV. It uses Frequent Batch Auctioning (FBA) to prevent MEV frontrunning, thus making the transaction fees for users lower, and a large portion of MEV value is captured and redistributed to SEI token holders, validators, and delegators.

While currently showing the lowest block-producing validator count, Sei aims to improve decentralization through zero-knowledge light clients, enabling broader blockchain verification.

Current Ecosystem Status

Despite launching before Sui, Sei's ecosystem shows more limited adoption:

52K active addresses (versus Sui's 1.1M)

$149M TVL (approximately 15% of Sui's)

Ecosystem dominated by standard DEXs and money markets

Some of the more interesting apps include DragonSwap, a DEX. DragonSwap where stakers share in the revenue through a fee switch and receive airdrops. The DEX also is looking to integrate a predict-and-earn platform.

Another interesting category of development is perpetual DEXs like Filament and Vertex. Sei’s speed enables perpetual DEXs. However, the competition in this product category is increasing with dApps like Sui’s DeepBook and HyperLiquid.

With Sei, the intrigue lies not in its current ecosystem, but in its ambitious vision for the future.

With Sei, the real interest lies not in its current ecosystem but in its future plans.

Future Development Initiatives

Sei is actively working to expand its ecosystem through several funding programs:

Sei Creator Fund (with Gitcoin):

$10M fund launched June 2024

646 applications (exceeding Sui's Overflow Hackathon)

Categories of focus include:

Creative media and IP development (e.g. lore around Sei)

Decentralized content platforms

NFT marketplaces and tools

Social Platforms and fan engagement

Decentralized crowdfunding

Web3 creative tools and infrastructure

Creator DAOs and collectives

Web3 content discovery, creation and curation

Web3 skill-sharing and education

Million Japan Ecosystem Fund:

$50M fund launched July 2024

Targeting Japanese startups in gaming, social, and entertainment

Part of broader Asian market strategy

User Engagement Programs:

Sei GG: The Legendary Gauntlet offering $50,000 in prizes for Web3 gamers

The impact of Sei’s ecosystem development funds remains to be seen. For now, Sei offers limited engagement opportunities, positioning it as a high-performance, general-purpose Layer 1 still in search of a standout use case or key partner to drive wider adoption.

In sum, Sei’s DeFi-focused design gives it a solid foundation, with features like EVM compatibility and MEV management aimed at setting it apart. While its user base and ecosystem adoption lag behind competitors like Sui, Sei’s funding programs and developer incentives indicate a serious push for growth. Ultimately, Sei’s potential as an alternative to Solana depends on its ability to expand beyond DeFi and attract a broader range of users and applications.

Enterprise Strategy & Developer Focus – Case: Aptos

Like Sui, Aptos was founded by former Meta employees, however, it takes a much more Web2-centric approach. Partnering with Microsoft on AI model training and exploring use cases like CBDCs, Aptos minimizes crypto ideologies. This is its greatest strength and weakness.

Aptos has a straightforward selling point: it's the "fastest" L1 with a time to finality of 200ms and employs a more secure smart contract language, Move (which is also used by Sui, although Sui has developed its own adapted version). This unique design enables the creation of innovative dApps.

To attract Web2 brands, Aptos prioritizes straightforward onboarding for both users and developers, recognizing the challenge of promoting a new programming language in a market dominated by Rust and Solidity.

User Onboarding

Privacy-Preserving Accounts – The Move language allows users to create wallets that ensure privacy by enabling multiple accounts without inherent links

Aptos Connect – A keyless account system using OIDC accounts (e.g., Google, Apple), ensuring that Google account and wallet data remain unlinked

Petra Wallet – Merges Web3 wallet functions with features similar to Venmo/Revolut, such as reminders for debts. It also seeks to establish itself a curator via Petra Drops (received NFT drops from creators you want to engage with) and Petra Groups (create communities around interests). Basically a Phantom wallet competitor.

Kana Labs Paymaster – Allows dApps to cover transaction fees, enabling free transactions for users

Developer Onboarding

Aptos Build – A Web2-like developer dashboard that allows users to deploy NFTs with a click or generate APIs. The goal is to make Aptos the chain on which it’s easiest to go from 0 to 1 in app development.

Aptos Build Aptos Learn and Overmind – An interactive tutorial and quest platform for developers

Aptos Learn

Overmind

Aptos Assistant – An AI chatbot addressing Aptos-related queries, including smart contracts

Strategic Partnerships and Ecosystem

While other blockchains often prioritize Web3 users, Aptos takes a distinctly Web2-focused approach through key partnerships:

Microsoft Azure powers the platform's AI chatbot

Microsoft, SK Telecom Co. and Brevan Howard collaborate on Aptos Ascend enterprise platform

BCG helps financial institutions implement Web3 and digital asset solutions

NBCUniversal develops fan experiences and games using their IP

Marketing through Web2 partnership announcement

This Web2-first approach comes with clear trade-offs. Aptos Connect includes strict terms and conditions, such as VPN restrictions (a questionable choice considering the security benefits VPNs provide for Web3 users) and explicit data collection policies – choices that may alienate crypto natives while appeasing traditional businesses.

Current Ecosystem Status

Despite its Web2 focus, Aptos features some intriguing applications. Naturally, the most popular ones are partnerships with Web2 companies rather than apps built from the ground up:

Consumer & Gaming:

STAN – An Indian esports and influencer platform

Chingari – Known as the TikTok of India, it allows users to earn GARI through app interactions and accounts for 80% of daily active users and 50% of gas fees paid on Aptos since switching from Solana

Overlai – Adds invisible watermarks with creator credentials on images, documenting ownership on the Aptos blockchain

KYD Labs – An event ticketing platform built on Aptos

Tapos – A clicker game that serves as a proof of concept for bot activity, though lacking depth in gameplay

DeFi

Aries Markets – The leading margin trading protocol by TVL

Merkle Trade – Gamified trading platform with NFT-based trading benefits

TradFi

Aptos Ascend – Compliant and permissioned platform for traditional finance, comparable to Sui's Closed-Loop Token Standard and Solana’s Token Extensions.

Privacy Features (In Development):

Compliant Confidentiality: Hidden payment amounts and sender/recipient identities

Concealed Auctions: Protected bidder information

Privacy-Preserving DEXes

Community Efforts

Aptos fosters community engagement through initiatives like the Aptos Collective, an ambassador program encouraging active participation, and the Aptos Forum, a central hub for discussions around the ecosystem.

Also, similar to the other Layer 1s, Aptos is implementing grant programs and hackathons to support developments in the areas of:

DeFi/RWA

Gaming/NFTs

AI/DePIN

Social

The Unexpected

Market Context

Over the past few years, blockchain industry has witnessed the rise and fall of several "Web2 blockchains" like Polygon, Flow, Palm, and Tezos. Their brief success and subsequent decline reveals how corporate blockchain enthusiasm often fades before meaningful adoption takes hold. This pattern becomes particularly relevant today, as Web2 brands increasingly explore launching their own Layer 2s to capture control and sequencer revenues. Rollup-as-a-service platforms like Conduit have made this path easier than ever before.

Aptos enters this landscape with an ambitious vision: creating a closed ecosystem of decentralized applications (dApps) and hardware around its blockchain, reminiscent of Apple's strategy. This approach requires significant upfront capital investment in infrastructure to foster a thriving ecosystem. While the strategy could yield powerful network effects if successful, it carries considerable risks.

The true test for Aptos lies in retaining users and developers over time, converting headline-grabbing partnerships into genuine adoption. This challenge grows as CEX-linked Layer 2 blockchains like Base (Coinbase) and X Layer (OKX) emerge with built-in liquidity advantages. Meanwhile, projects like Movement Labs are bringing the Move programming language to EVM, potentially diluting Aptos's technical edge.

The current ecosystem raises critical questions. Many applications remain in early development stages, and existing engagement appears largely incentive-driven. The case of Chingari illustrates this challenge – users reportedly keep the app running in the background solely to earn tokens, suggesting partnerships haven't yet translated into meaningful utility.

In contrast, Solana has pursued a user-centric path. While also engaging with Web2 brands, Solana prioritized organic adoption, building infrastructure iteratively around actual usage patterns. This bottom-up approach to ecosystem development may prove more durable than Aptos's top-down enterprise strategy.

The fundamental question for Aptos extends beyond technical capabilities: Was Move created for blockchains, or were blockchains created for Move? This distinction reflects a deeper tension between technological innovation and practical adoption. While Aptos's enterprise-first approach might stem from years of Move development, success will ultimately depend on whether it can overcome the historical challenges that have faced previous corporate blockchain initiatives and establish lasting market presence.

Community-Driven Evolution – Case: Monad & Berachain

Layer 1 success requires more than just technical superiority. When Base launched in August 2023, it was slower than 22 other blockchains in max TPS, yet achieved greater adoption and revenue than many technically superior chains. Even Arbitrum boasts faster speeds than most new L1s, and Unichain will soon have faster block times than all except Aptos. The lesson is clear: to avoid becoming the next EOS or Canto, new L1s need something beyond performance metrics – they need vibrant communities of users, developers, and ambassadors who make the chain compelling to build on.

Historically in crypto, a great cult beats great tech (just ask Murad). Cardano and XRP, despite questionable technical merits, have consistently outperformed more advanced chains like Cosmos and Polkadot in market cap through cult-like followings. While market cap alone doesn't define success, it drives a powerful feedback loop: higher valuations mean larger treasury assets and increased attention from both users and businesses. Even Solana's early success came despite its tech (frequent outages and dropped transactions), carried by strong community backing.

This is where Monad and Berachain's opportunity lies. While Sei, Aptos, and even Sui have a distinct "VC chain" feel, these newer L1s (despite backing from many of the same VCs) are cultivating authentic community engagement. The combination of great tech with cult-like following is particularly powerful.

The strategy makes particular sense when you consider Web2 partnerships. While it would seem to make sense to go directly for Web2 brand partnerships, you have to remember who actually serves as the first users and testers. Unless a brand is ready to put its entire operations onto the blockchain from day one, which historically hasn't been the case, the first users will always be a Web3 native audience. Without such an audience, Web2 brands are likely to deem their blockchain experiments instant failures.

To attract these users, chains need compelling utility. Financial upside remains the strongest draw (part of why Ethereum's narrative is currently struggling), but there's also power in community status, or the ability to gain recognition through responsibilities, partnerships, and Discord roles. This maps directly to Maslow's upper hierarchy: esteem and self-actualization through community participation.

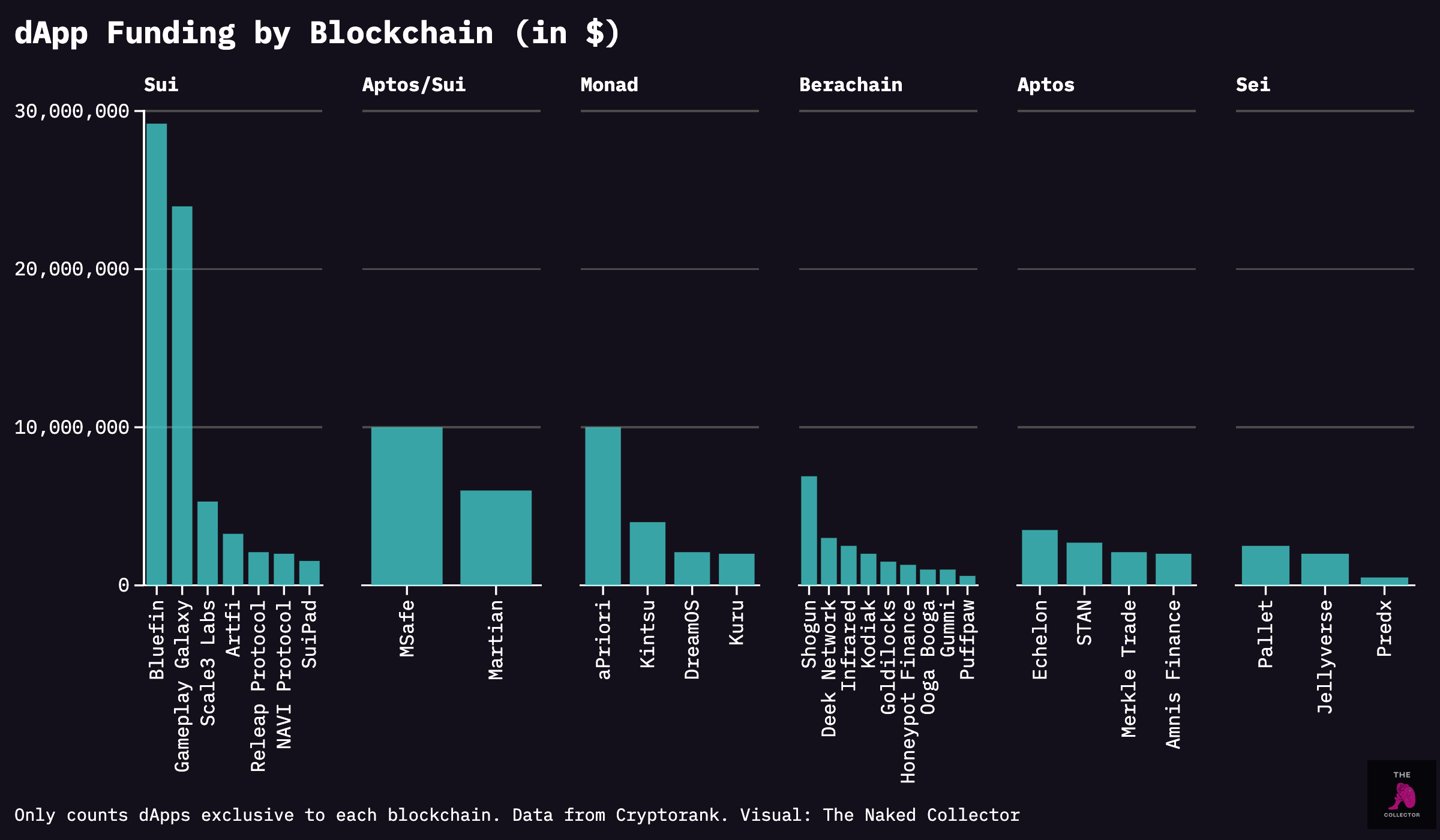

This community-driven approach seems to be working as Monad and Berachain dApps are receiving more funding than Aptos and Sei combined, despite not even reaching mainnet (or in Monad's case, testnet).

Monad – The Culture Chain

While Monad has impressive tech, its ability to engage its community is even more impressive. This becomes even more notable when you consider it hasn't even reached testnet launch. Community engagement will need to remain strong since, looking back at the new L1 metrics comparison, Monad doesn't outperform all the other chains and the benefits of EVM compatibility remain to be seen.

Its biggest advantages come from elsewhere: strong community fit, natural alignment with consumer apps, and feeling more like an actual application than just another boring infrastructure play.

Monad has already built a substantial community with over 373K Discord and 26.6K Telegram members, crucial for ecosystem growth. Unlike many crypto Discord servers where communication feels haphazard and random, Monad gives real meaning to community participation.

This community focus shows up in their initiatives like the Run Club and MonLingo language-learning project. These efforts aim to foster organic growth and strengthen connections within their user base all over the world.

Their Twitter strategy shows the same thoughtful approach, with different accounts serving distinct purposes:

@monad_xyz for official updates

@monad_eco for ecosystem highlights

@cryptunez and @intern for marketing/memes

@pipeline_xyz for video and podcast content

Even their official Twitter takes a refreshingly different approach with timely memes, often featuring their community-created mascot, the Molandak. Where Sui, Aptos and Sei's meme efforts feel calculated, for Monad it's part of their core identity.

This, in turn, leads to engaging Twitter performance metrics.

They bring this community-first approach to everything they do. The Monad Madness $1M pitch competition was streamed live on Twitch, making the community part of the journey. And while Sei, Sui and Aptos chase backing from trading firms and Franklin Templeton, Monad brought in Web3 natives like Cobie, Hsaka, Ansem, Luca Netz and eGirl Capital. This choice of backers lets them stay authentic and not take themselves too seriously when building community.

Instead of running after Web2 partnerships, Monad is turning inward towards its community. They're breaking down the barrier between user and organization, much like Solana did and something Ethereum still has had a tough time doing.

Consumer dApps

What's striking about Monad's ecosystem isn't just its technical capabilities, but rather the experimentation happening within it. Instead of focusing solely on perpetual DEXes (which you might expect given the chain's parallel processing), Monad is attracting builders interested in pushing Web3's boundaries into new consumer territories:

Gamified Trading & Betting:

LEVR Bet – First decentralized leveraged sports betting platform, offering up to 5x leverage. The real-time betting mechanics specifically leverage Monad's speed advantages.

Kizzy – Social betting platform targeting cultural phenomena and influencer events

RareBetSports – Advanced sports betting focusing on individual player stats, with plans for esports integration

TradingLeagues – Gamified approach to stock and crypto trading

Consumer Applications:

Plato – Gamified dining experience where users earn $FAT tokens through restaurant visits and food-related quests

Boujee – Luxury fashion platform combining social features with loyalty rewards (to understand why this has potential see my fashion & luxury loyalty report here)

NoMoreLonely.Life — Dating platform built on-chain

Gaming:

Anterris – Action RPG with breeding mechanics, developed by ex-Riot Games team members

DeFi:

Development Strategy

The platform's project pipeline centers on its Monad Builder Programs:

Monad Madness: $1M pitch competition co-hosted with Paradigm for early-to-intermediate stage projects

Mach: Monad Accelerator for early-stage projects

In addition, Monad takes a pragmatic approach to infrastructure, partnering with established Web3 players rather than building everything from scratch. Key partnerships include Phantom and OKX for wallet integration and distribution.

A Competitive APAC Focus

Monad is placing a strong emphasis on the Asia-Pacific region, which is crucial for its growth strategy:

APAC community leads driving regional engagement

Collaboration with Neowiz, an online game publisher in South Korea, on the blockchain gaming platform Intella X, including a crowdfunding platform on Monad

Partnership with Hex Trust, a Hong Kong-based digital asset custodian, for institutional-grade custody

The second Monad Madness competition will be hosted in Bangkok.

Similar to Monad's focus, competitors are also targeting the APAC region:

Sei: Focused on building the Million Japan Ecosystem

Sui: An official conference partner for Korea Blockchain Week 2024 and partnered with TikTok subsidiary Byteplus

Aptos: Acquired HashPalette, a developer of the Palette Chain in Japan, and formed partnerships with SK Telecom and Lotte, two major South Korean entities

Berachain: Actively recruiting a growth lead in the region to bolster its strategy

Culture as a Competitive Advantage

The analysis of Monad highlights a distinctive strategy: while it offers capable Layer 1 infrastructure, its edge against Solana is rooted in cultural engagement and consumer-focused applications rather than broad technical superiority. Monad's community-driven initiatives, along with strategic Twitter engagement, foster authentic relationships with its user base, emphasizing participation over mere infrastructure.

Monad’s greatest strength lies in its culture, which not only motivates founders to build but also creates a loyal “plug-and-play” community eager to test new protocols. This active engagement opens up the design space for the types of projects that can find success on Monad, particularly in lifestyle-driven applications like gamified dining, decentralized dating, and digital-to-physical products, where we are already seeing internal product-market fit with the Monad Run Club. While other blockchains may rely on incentivization via high yields or existing Web2 app users, Monad has the ability to think outside the box.

However, Monad’s journey underscores a crucial point about competing with Solana: a compelling Layer 1 requires more than just throughput. While its architecture supports advanced DeFi and gamified platforms, its true strength lies in nurturing a culture that resonates with early adopters. Monad’s biggest challenge will be to maintain this “memetic premium” even after tangible projects start launching on the blockchain, avoiding the typical “buy the rumor, sell the news” pitfalls that often plague Web3.

Berachain — Memetic Tokenomics

Unusually, Berachain began as an NFT project, Bong Bears, in August 2021 and is currently on a testnet, with a mainnet launch expected by the end of 2024. To date, over 200 teams are building on Berachain, boasting 400k active addresses and processing 34 million transactions on its testnet. The project is valued at $1.5 billion following a $69 million funding round led by Brevan Howard Digital and Framework Ventures.

Like Monad, Berachain differentiates itself not only through technology but also through effective brand building. It has attracted 468k Discord members and 23.3k Telegram users, maintaining strong engagement on Twitter.

The marketing strategy targets Gen Z users, utilizing short videos and YouTube thumbnail-like cover art, creating an image more akin to a memecoin than a conventional Layer 1. This branding shines through not only in communications but also in project names, often featuring bear-related themes.

A striking feature of Berachain is its tokenomics which aim to solve the liquidity fragmentation problem in crypto. At the core, it employs a proof of liquidity consensus mechanism designed to align governance with validation, moving away from the traditional "mercenary" validator model.

Innovative Tokenomics

Validators earn soulbound governance tokens (BGT) instead of gas tokens, but they can burn BGT for BERA, the gas token. They distribute their voting power across reward vaults, deciding which liquidity pools receive BGT rewards. Think of BGT as loyalty tokens that capture more value as the brand grows.

This structure aims to create a liquidity flywheel where liquidity providers gain an increasing stake in the underlying Layer 1 – a win-win scenario.

In practice this reminds a lot of the Curve bribe wars. Instead of locked up veCRV we have the soulbound BGT and instead of “bribes” we have “incentives” to attract BGT emissions from validators.

The risk here lies in the potential for validator centralization. To become a validator, you need a minimum of 69,420 BERA tokens, the gas token for Berachain. Although the price of BERA remains uncertain until its launch, it is likely to be costly. Validators can then direct reward, using their BGT governance tokens, to liquidity pools where they provide liquidity. In return, they not only earn LP rewards but also accumulate more BGT, reinforcing their own influence and consolidating power. This dynamic incentivizes protocols, such as reward vaults, to inflate their incentives or APYs, potentially to unsustainable levels, favoring vaults offering, say, 200% APY over those providing a more modest 10%.

On a brighter note, this model could democratize the Berachain network, enabling direct ownership and governance by users (or by proxy if BGT is delegated). Currently, third-party projects like Lido profit significantly from blockchain validation. Berachain aims to redirect those earnings straight to its users.

A higher BERA price could drive increased liquidity through greater LP incentives and more demand for governance tokens, strengthening the validator network. Conversely, a lower price could have negative effects. Berachain hopes to succeed where other DeFi projects, like Olympus DAO and Redacted Protocol, have stumbled.

dApp Ecosystem

True to its nature, Berachain has attracted innovative projects.

Some of the most interesting ones include:

Consumer:

Deek Network – A decentralized collaboration platform that enables users to share knowledge, build on-chain reputations, and monetize social interactions through its innovative "Wishes" system and upcoming $DEEK token. Powered by OpenSocial, a protocol for building Web3 native dApps.

Puffpaw – A DePIN vape-to-earn project that rewards users for using lower-nicotine cartridges to help reduce their nicotine dependence.

DeFi:

Honeypot Finance – An on-chain accelerator that combines a fair launchpad with a secure DEX

Gummi – A platform that enables users to create money markets for any pair within minutes.

The primary pipeline for new projects is the official Berachain ecosystem incubator, Build-a-Bera, which provides seed funding, mentorship, workspace, networking, resources, and recruiting support.

Much like Monad, Berachain presents itself as an integrated application ecosystem rather than mere background infrastructure. The bear-themed branding provides immediate recognition for projects, creating a shared lore and allowing for the reuse and remixing of brand elements and mascots, which fosters a more cohesive marketing strategy.

Placing the user community at the core of the product is an advantage but also a responsibility for both Monad and Berachain. They will have tread a fine line, balancing the needs of their community with the expectations of major VC funds that have bid up their valuations into the billions ($3B for Monad and $1.5B for Berachain). Few things demoralize users and retail investors more than token unlocks—typically low-float, high FDV coins—driving the token price to the ground.

While the issue of low-float, high FDV has been widely discussed, it has contributed to the underperformance of recently launched protocols like Wormhole (26% MC/FDV) and ZKsync (17.5% MC/FDV).

Ultimately, these two Layer 1 solutions have discovered that the best way to combat tech centralization is by embodying the opposite approach of the brands they seek to differentiate themselves from.

The Modern Gold Rush – Novelty Creates Opportunity

In addition to blockchain-specific advantages and disadvantages, a few external factors are at play.

In a landscape dominated by established players like Solana and Ethereum, new Layer 1s present a unique opportunity for builders and investors to become the “big fish in a small pond.”

This shift has three significant implications:

Emergence of Smaller L1-Specific Venture Funds: New Layer 1 ecosystems, like Berachain, will foster the rise of specialized venture funds focused exclusively on these platforms. These funds will fill a critical gap by supporting smaller projects that may not attract the interest of major players like a16z or Paradigm. While top-tier VCs dominate the most lucrative deals, emerging funds can gain prominence by concentrating their investments in specific ecosystems just like Multicoin Capital did within the Solana ecosystem.

Increased TradFi Investment: Traditional finance is will likely to engage more actively with emerging Layer 1 chains, leveraging partnerships for financial gain. For instance, firms may fund a Layer 1 project, establish a partnership, and subsequently earn carried interest. Notable examples include Flow Traders investing in Sei, Franklin Templeton backing Sui and Aptos, and PayPal supporting Aptos.

Retail Engagement and the Search for Opportunity: Retail investors will flock to new ecosystems in search of financial opportunities, often remaining loyal to the blockchains that provide tangible rewards. While some may criticize the financialization of crypto, incentives are essential for exploring these new frontiers. Much like the California Gold Rush, opportunities must exist for users to find "gold," which represents not only financial gain but also autonomy, freedom, and a sense of belonging. The financialization of both the Gold Rush and today's crypto markets attracts infrastructure development on these new frontiers.

For various Layer 1s, this metaphorical gold rush could manifest in different ways:

Sui aims for a Solana-like memecoin cycle that translates into a vibrant ecosystem

Aptos and Sei hope that traditional finance will adopt their protocols, with retail users sticking around

Monad seeks to transform memes into culture, fostering the development of Monad-specific dApps

Berachain anticipates that innovative tokenomics will enrich its contributors, creating a flywheel of attention and activity

Two Contrasting Futures

Looking ahead, two contrasting visions for Layer 1 functionality emerge:

Modular Thesis – A UI layer, such as Infinex or Particle Network, abstracts the underlying Layer 1s, allowing brands to utilize their own modular chains. dApps operate independently of these blockchains, executing transactions on the most suitable one for each case. This commoditizes Layer 1 branding, favoring only the most performant chains. In this scenario, ecosystem development and community building become less significant.

Winners: Aptos, Sei, and possibly Sui.

Monolithic Thesis – Most users and dApps will gravitate towards a few dominant chains that offer the best and most engaging user experiences. For instance, Uniswap has maintained a significant share of DEX transaction volume despite the emergence of aggregators like 1inch, while users continue to prefer wallets like MetaMask and Phantom for swaps, even at higher fees. This concentration of activity follows a power law distribution, rendering many other UIs irrelevant.

In these thriving communities, intangible factors such as branding and community building become crucial. If users are accustomed to and enjoy Berachain-branded apps, they are unlikely to switch to cheaper alternatives. User loyalty, relationships, and trust are significant factors; once captured, they create strong barriers to switching. Well-designed consumer-facing applications are challenging to abstract away.

Winners: Monad, Berachain

To summarize the competitive dynamic between these new L1s and Solana, two distinct approaches are emerging. One path, taken by Aptos and Sei, emphasizes technical excellence and institutional adoption. The alternative strategy, pursued by Monad and Berachain, focuses on community and culture, betting that strong brand loyalty and user experience will prevent commoditization. Sui sits interestingly between these approaches.

These emerging L1s aren't just competing on performance metrics – they're racing to establish strong network effects before Solana becomes more technically capable. Whether through Sui's gaming ecosystem, Aptos's enterprise partnerships, Sei's DeFi focus, or Monad and Berachain's community-first approach, each is betting that their chosen path will help them achieve the Lindy Effect first. Success likely won't come from out-engineering Solana, but from building lasting communities and use cases that keep users engaged regardless of technical specifications.

IV. Why Solana May Still Outperform

While this report focuses on emerging Layer 1s, Solana maintains several unique advantages that make it difficult for competitors to capture market share.

Product Strategy and Ecosystem Strength

Solana excels at product promotion and has established itself as the 'Apple of Web3' for its consumer-friendly approach and brand appeal. Its ecosystem hosts some of the most interesting applications, particularly in the DePIN (Decentralized Physical Infrastructure) sector, where projects like Hivemapper (founded in 2015), Helium (founded 2013), DIMO, DAWN, and Render have inherent moats due to the long development timelines required to scale infrastructure.

Moreover, Solana has captured the attention of both TradFi institutions and crypto investors alike, evidenced by backing from firms like Multicoin Capital.

Technical Foundation and Market Positioning

While other Layer 1s chase high specs, Solana has achieved fast, affordable performance that’s “good enough” to sustain diverse applications, from consumer-focused apps to memecoins. With ongoing improvements like Firedancer, Solana is targeting up 600K–1.2M transactions per second (for context, Visa averages 1.7K TPS and Nasdaq 20K traders per second), positioning itself to unlock emergent, high-traffic use cases. This practical approach, bolstered by a first-mover advantage among monolithic blockchains, has drawn both retail and institutional interest.

Strategic Differentiation

Unlike newer Layer 1s crowding into perpetual and order-book trading (competing with the likes of dYdX, Hyperliquid), Solana focuses on consumer applications and TradFi integration. Solana’s Token Extensions offer compliance features like privacy-preserving transactions and fund control—capabilities that have earned approval from TradFi leaders such as PayPal.

Developer Mindshare and Innovation

Solana is gradually winning over developers and investors from the Ethereum ecosystem. The migration of established projects like Sky (formerly Maker) could set a precedent for protocols shifting from EVM to SVM. Similarly, Parallel's decision to build its AI-powered game on Solana, despite having existing assets on Ethereum and Base, signals growing developer confidence.

Hardware Ecosystem Potential

With hardware products like the Seeker phone and PSG1 gaming console, Solana is creating a potential flywheel for consumer dApps. Though the initial Saga phone saw mixed reviews, it follows the path of Apple’s first computer—limited early traction but transformative potential. If Solana’s hardware continues to offer novel value to its core user base, it could disrupt the current mobile app market oligopoly.

V. What Do the Numbers Say?

While each new Layer 1 shows unique potential, let's examine what the metrics tell us about their current growth and popularity.

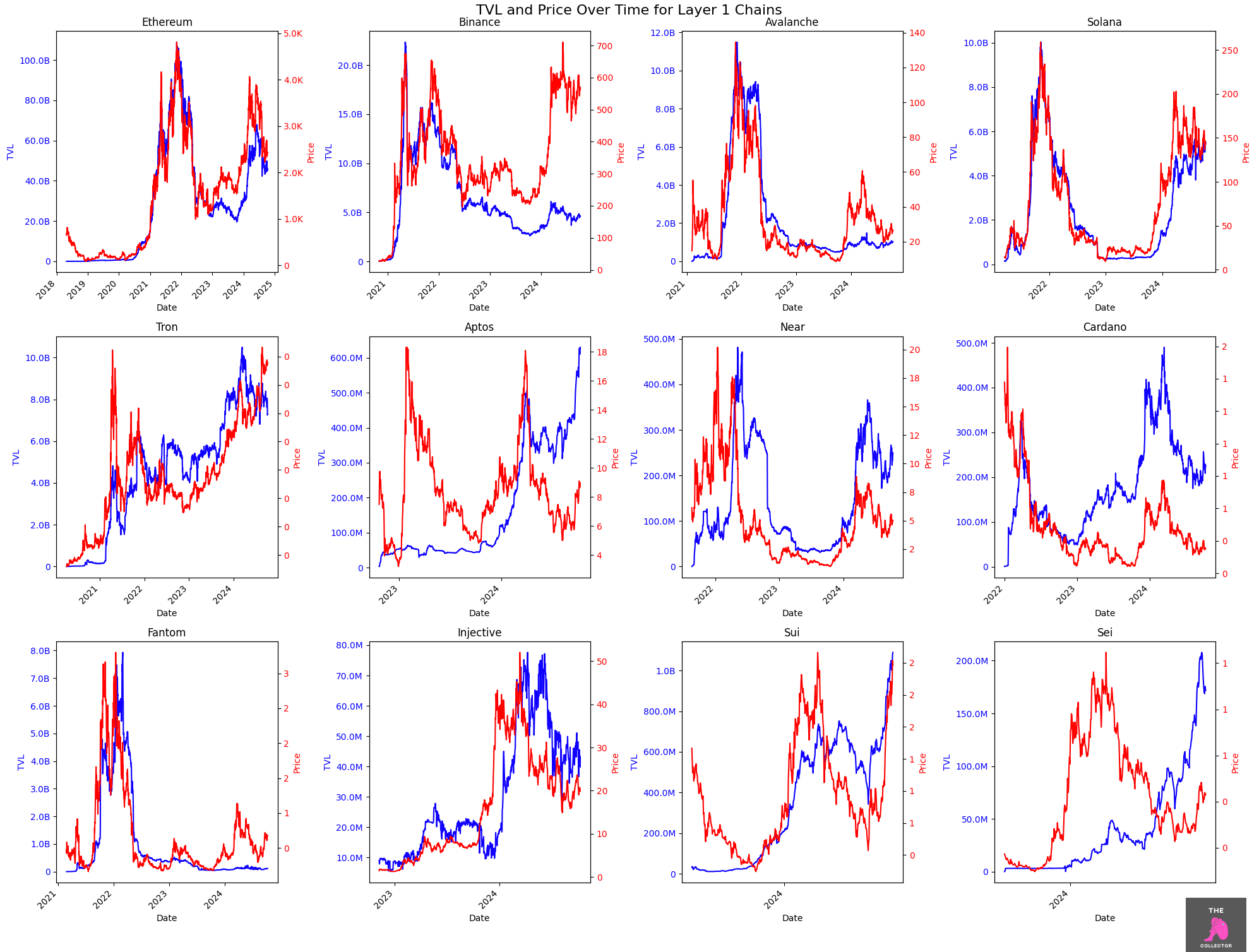

TVL Analysis

Solana currently dominates with 6x higher TVL than its nearest L1 competitor, Sui.

[Note: Monad and Berachain are excluded from most metrics as they haven't launched mainnet.]

However, the story becomes more nuanced when looking at growth trajectories. Sui has achieved higher TVL as a percentage of Total TVL a year after launch compared to Solana at the same stage, though by the 1.5-year mark, Solana had pulled ahead significantly.

When it comes to size and distribution of TVL, Sui is the leader while Sei is trailing by a lot. Aptos and Sei’s TVL is more concentrated in liquid staking while Sui’s is more concentrated in lending. Sui and Aptos have similar TVLs locked up in DEXes as % of their aggregate TVL.

TVL Distribution tells another interesting story:

Sui leads in overall size while Sei trails significantly

Aptos and Sei concentrate in liquid staking (~30% of TVL)

Sui focuses more on lending (52% vs competitors' 37%)

Sui and Aptos show similar DEX percentages

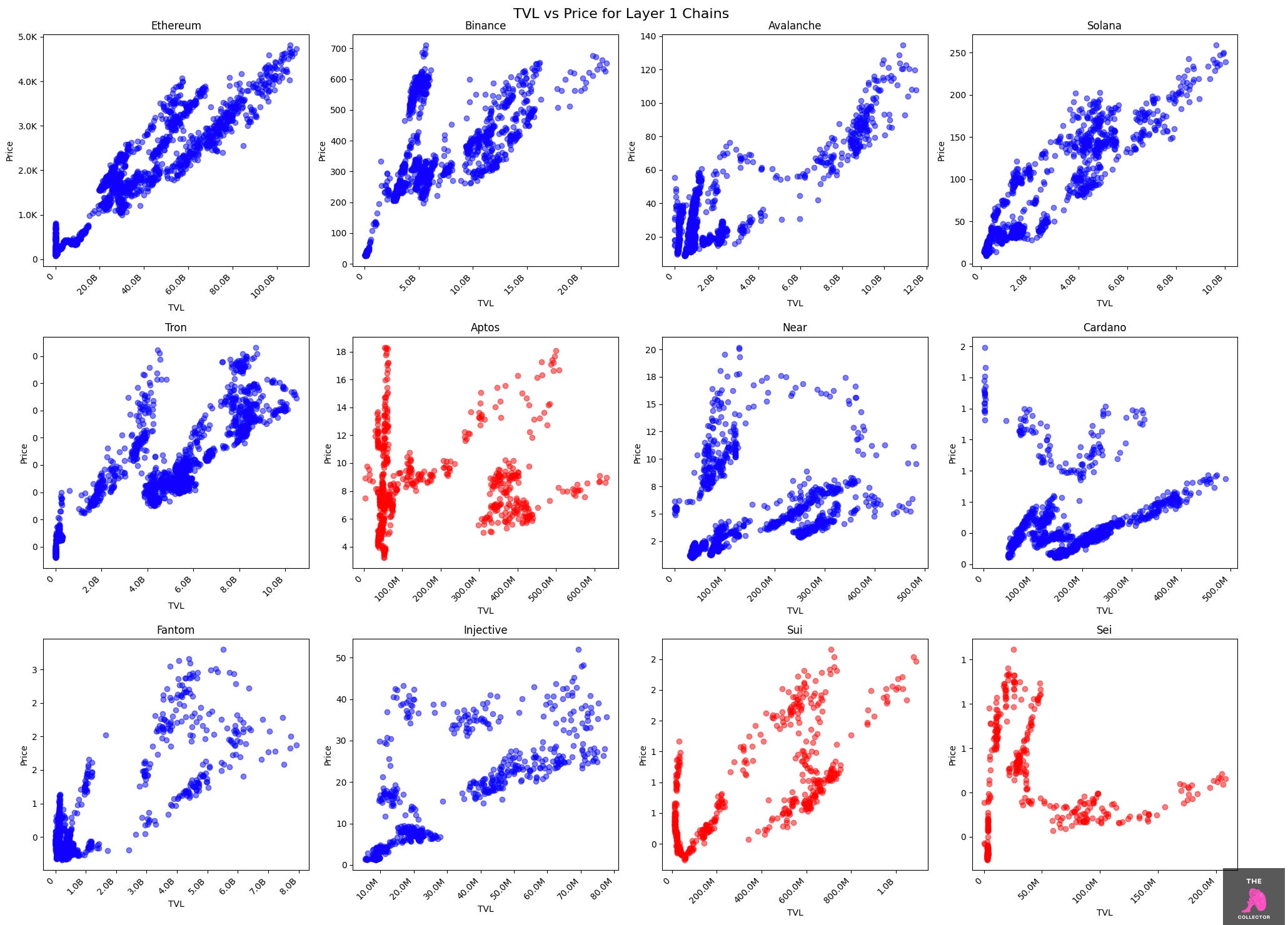

For those wondering about TVL-price correlation, the relationship is mixed. While established chains like Ethereum and Solana show strong correlation, newer L1s (Aptos, Sui, Sei) present a different pattern. These chains often launch "overpriced" relative to their TVL due to high initial valuations, and even as TVL grows, price hasn't yet caught up.

This hype around these new Layer 1s (Aptos, Sei, Sui) is further confirmed by overlaying price on TVL.

Activity Metrics

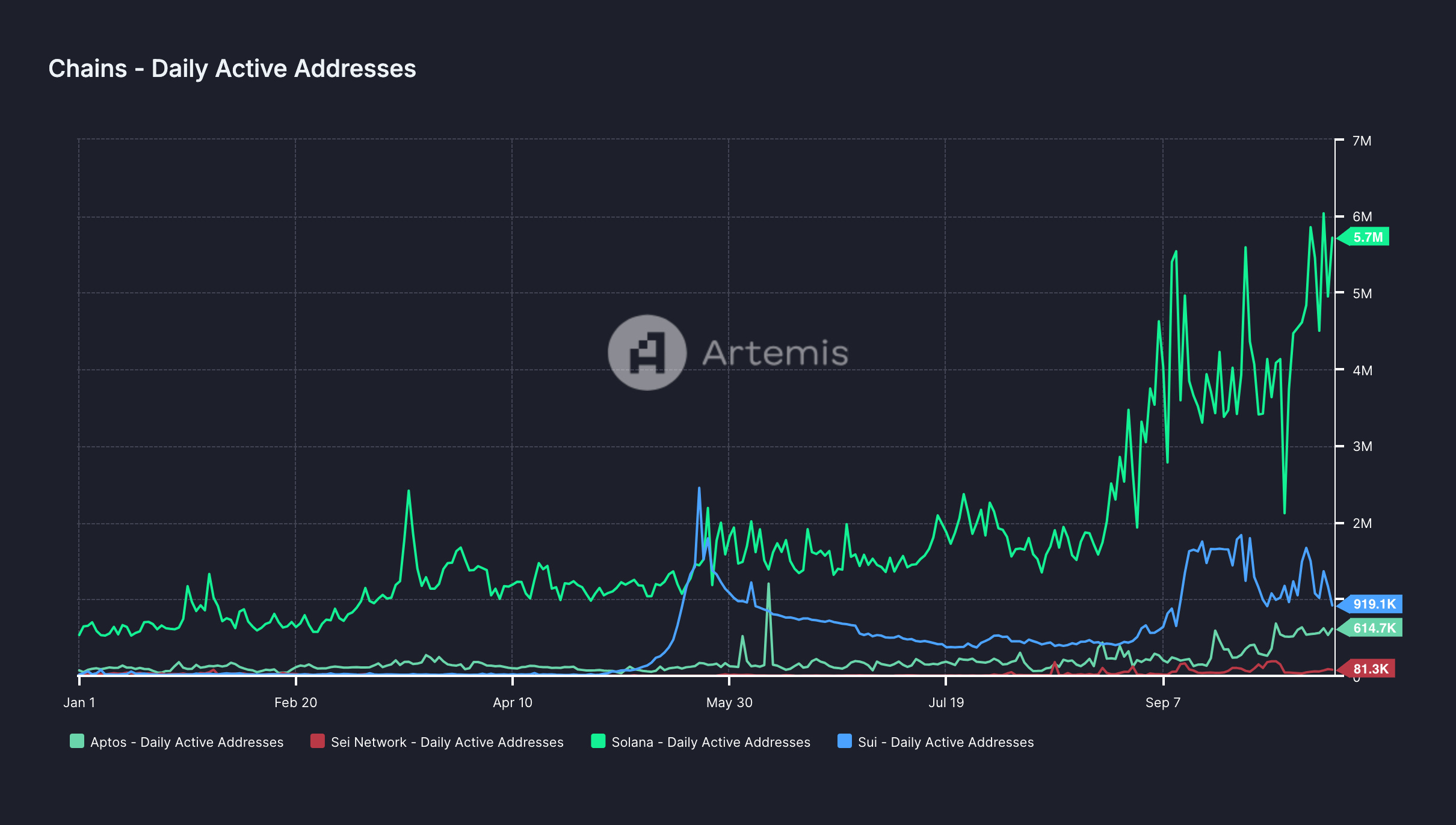

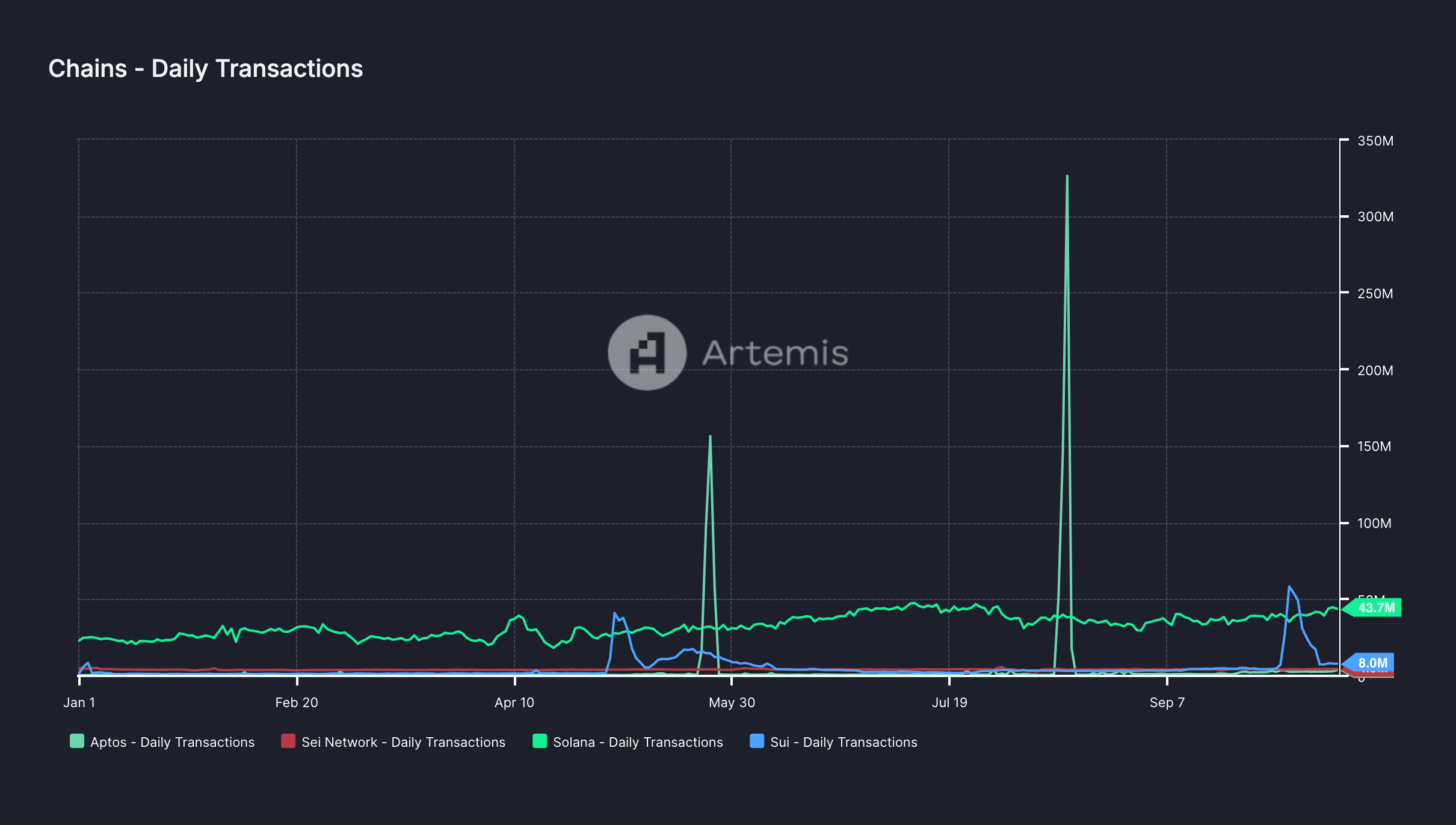

From an absolute value standpoint, Solana dominates user activity metrics, maintaining a 6x advantage over Sui in active addresses and 5.5x lead in daily transactions.

However, examining growth trajectories reveals a more nuanced picture. When comparing the first 500 days after mainnet launch, Sui actually shows stronger initial user growth than Solana did in its early days. This comes with an important caveat: overall crypto wallet activity is currently at all-time highs, providing a more favorable environment for growth.

Transaction data tells another interesting story. While Solana maintains clear dominance in daily transactions (5.5x higher than Sui), some activity metrics require careful interpretation. For instance, Aptos shows dramatic spikes in transaction volume due to the Tapos Telegram game - on August 15th alone, 210K users generated 330M transactions (1,552 transactions per account), suggesting significant bot activity rather than organic usage.

Historically, Solana retained higher transaction volume after 500 days pointing to higher usage per user.

In sum, while Solana clearly outpaces its competitors across most activity metrics, Sui emerges as the most credible challenger, showing growth patterns reminiscent of Solana's early days. However, it remains to be seen whether this is just hype and mercenary capital rotation or whether the blockchain will be able to sustain the users.

Tokenomics

Looking at token distribution across the new Layer 1s, we see remarkably similar patterns. Community allocations hover around 50-58% across Sui, Aptos, and Sei, while team and investor allocations range from 42-49%. Sui shows the highest community allocation at 58%, though the difference is relatively minor compared to Aptos (51.02%) and Sei (51%).

These balanced distributions suggest these Layer 1s are following similar tokenomics playbooks, likely aiming to strike a balance between community incentives and sustainable development funding.

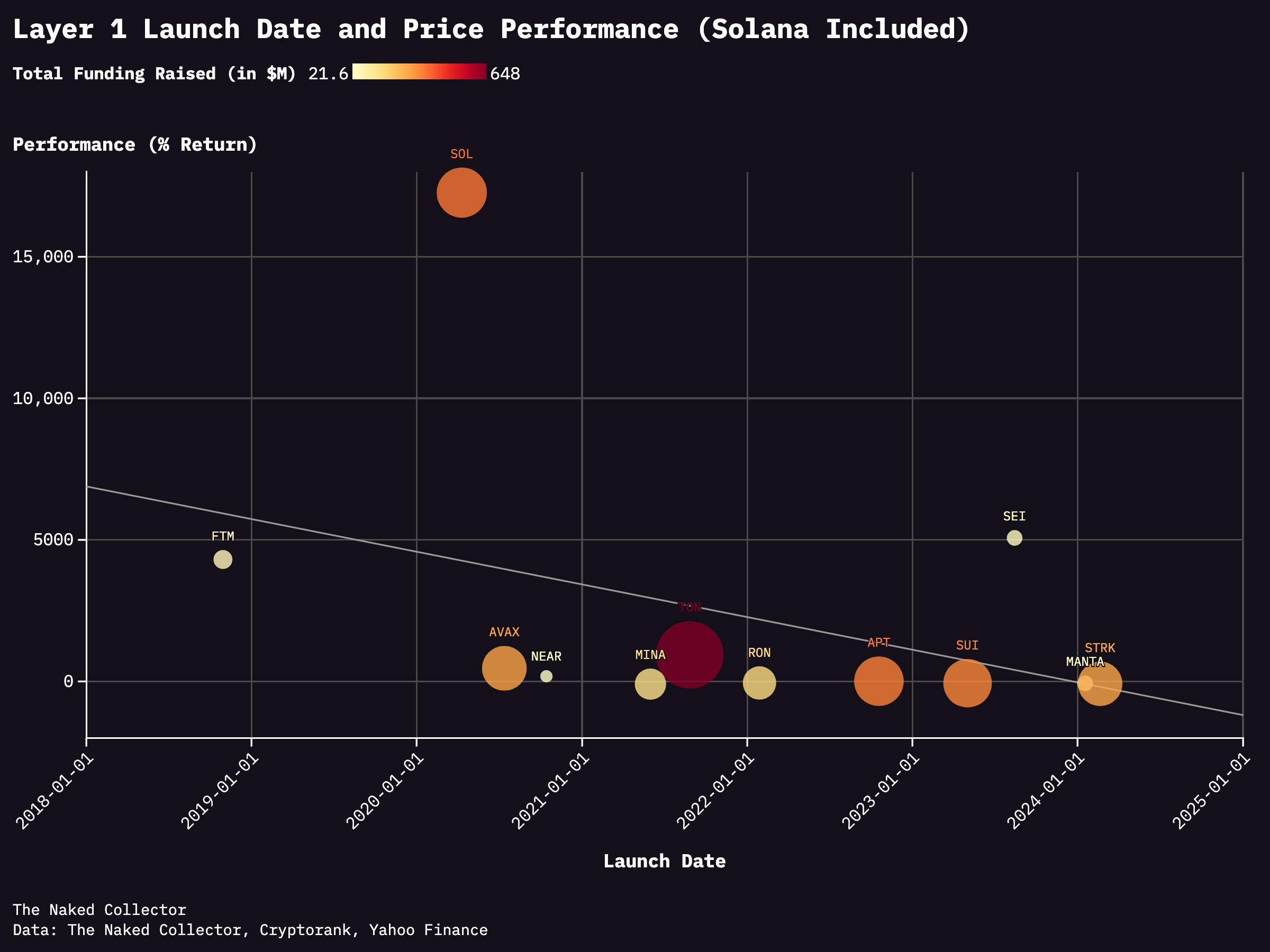

Funding Analysis

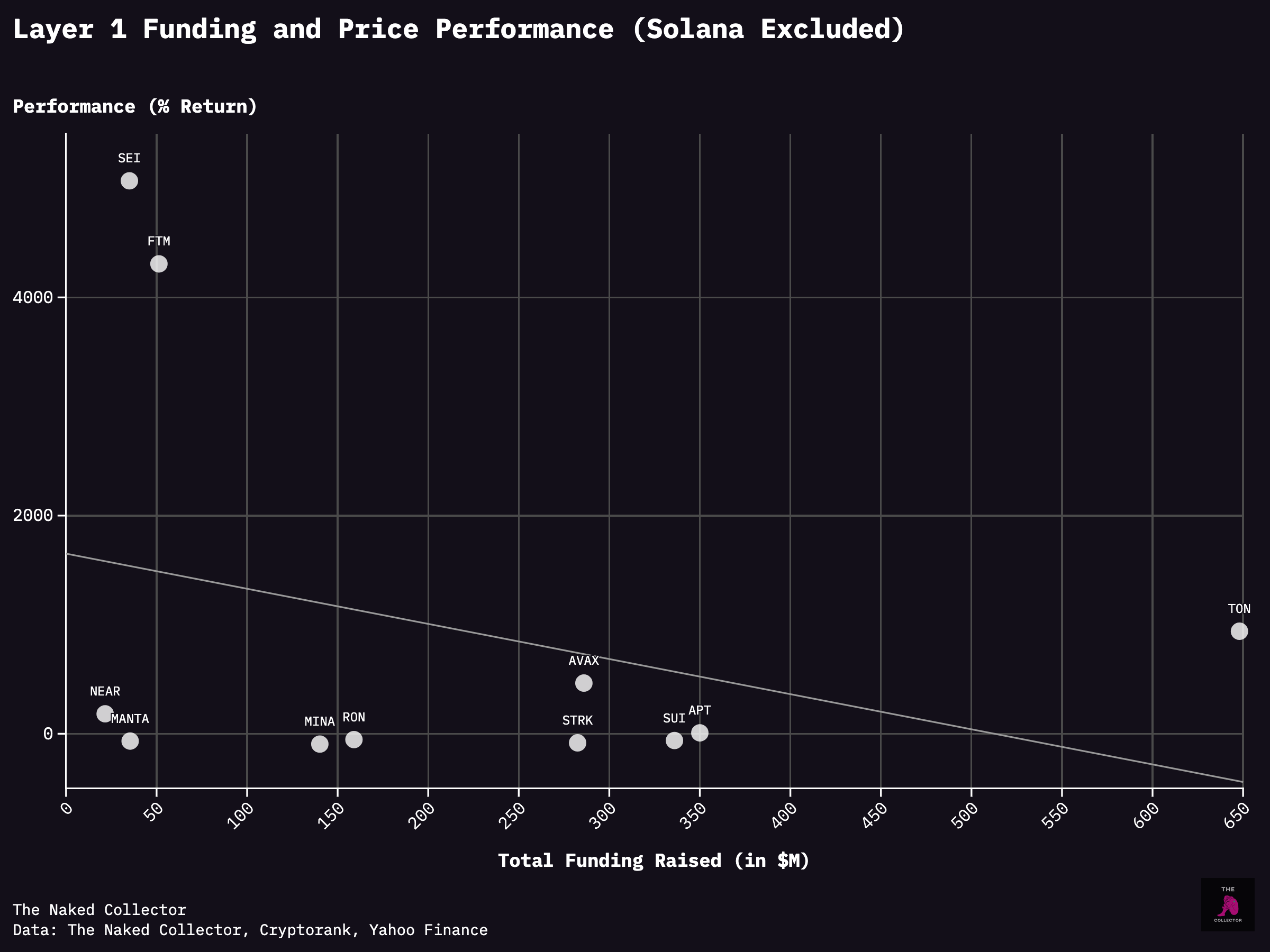

Sui and Aptos lead in funding raised, though timing played a crucial role. Sui began raising in late 2021's bull market, Aptos in early 2022, while Sei waited until August 2022 after the market crash. Monad and Berachain raised their rounds nearly simultaneously in 2023 and 2024.

Interestingly, larger funding rounds don't necessarily translate to better price performance. While including Solana shows a slight positive correlation, removing this outlier reveals a negative trend – suggesting that higher initial valuations might actually handicap public market performance.

Launch timing, however, shows more consistent impact. Earlier launches correlate with better price performance, whether including Solana or not.

While we can't yet assess Monad and Berachain's market performance, we can visualize them along the timeline, positioned for future launches.

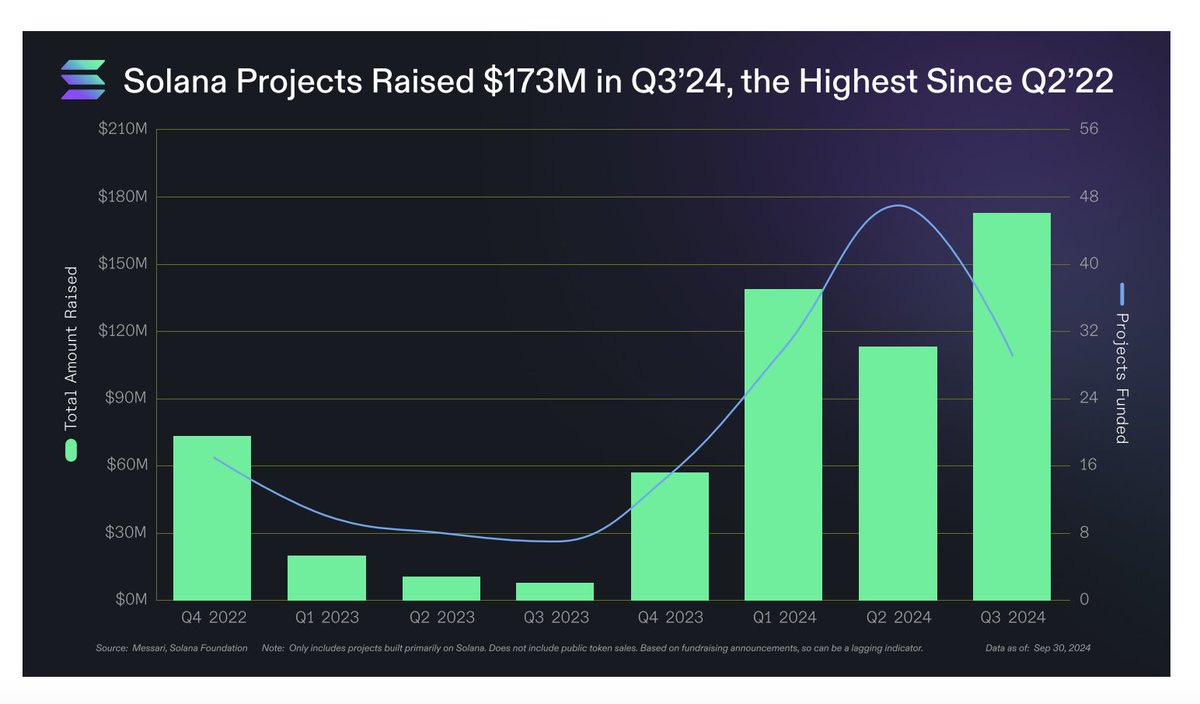

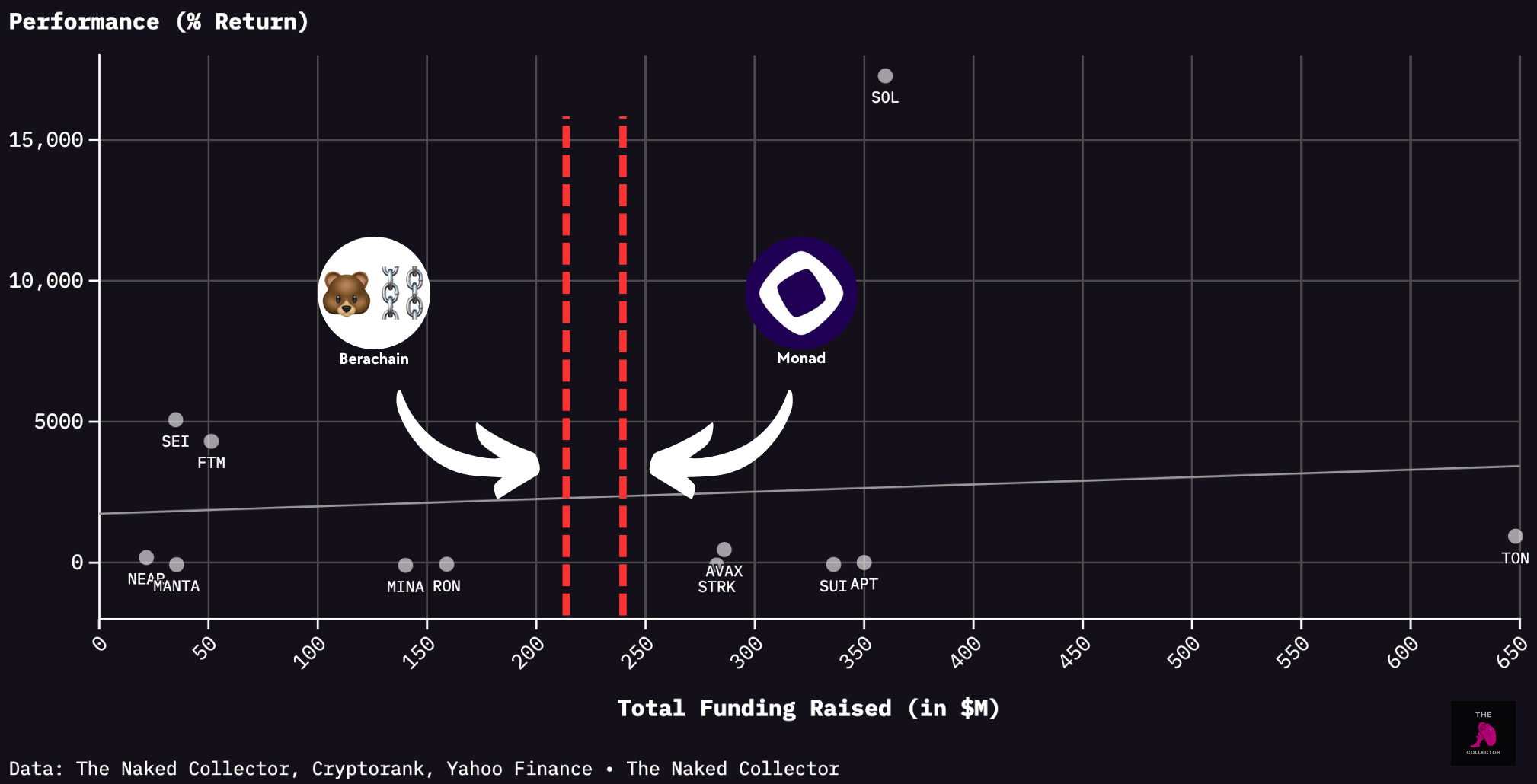

Looking at ecosystem funding tells another interesting story. While Sui leads among Layer 1s, there's a surprising twist in dApp funding: Berachain and Monad's native applications have secured more funding than those building on Aptos and Sei, despite neither chain having launched mainnet yet.

This level of pre-launch ecosystem funding suggests strong developer interest in these upcoming platforms, though as with other metrics, time will tell if this translates to sustained development activity.

Market Multiples

Multiples are often used to determine whether an asset is overpriced or underpriced relative to its competitors. Solana has the lowest multiples (making it the most undervalued) for DEX trading and NFT volume. However, it is the most overvalued when it comes to TVL (total value locked).

This indicates that Solana is popular for trading but less so for DeFi like lending markets, liquid staking or liquidity provision.

Here are the absolute numbers as of October 20, 2024.

Final Analysis

The metrics tell a clear story: Solana remains dominant across most measures, but Sui emerges as the most credible challenger. While Sui's growth trajectory impressively mirrors Solana's early days, it benefits from a more favorable market environment. An interesting disconnect appears in the funding data – despite Sui and Aptos leading in capital raised, there's no clear correlation between funding amounts and performance.

The ecosystem dynamics reveal surprising patterns. While Sui leads in overall ecosystem funding, Monad and Berachain's dApp ecosystems have generated more excitement than those of established chains. Meanwhile, new funding models are emerging through DePIN and DeVIN projects, with platforms like Aethir raising $135M from node sales compared to just $9M from VCs.

Yet, the critical question remains whether these newer L1s, particularly Sui, can convert their initial momentum and capital advantages into sustained user adoption and ecosystem growth beyond the initial hype cycle.

VI. Conclusion: The Future of Layer 1 Competition

Why Developer Experience Alone Isn't Enough

While many Layer 1s, like Aptos and Sui, focus on optimizing developer experience through new programming languages like Move, they face substantial hurdles, particularly the cold start problem. Meanwhile, generative AI tools like ChatGPT and v0 are reshaping the developer landscape, presenting an opportunity to create more successful Web3 dApps.

The intersection of developer experience and generative AI is crucial for the longevity and network effects of Layer 1s.

The Importance of Programming Languages

Blockchains that utilize prevalent programming languages will likely dominate, as generative AI models thrive on abundant training data. Languages like Python and Rust benefit blockchains like Solana. Conversely, Solidity has the richest context-specific data, favoring EVM-compatible chains. Move, although less contextually rich, offers safety features that could mitigate generative AI hallucinations. Notably, Aptos is actively developing generative AI tools with Microsoft’s support to seemingly leverage these advantages.

The Users = The Builders

The financialization of the crypto space opens opportunities for innovative dApp development, reminiscent of a potential “Pump.fun for dApps.” While complex DeFi protocols and AAA games require top-tier developers, simpler consumer dApps and minimum viable products can be developed more easily.

Unlike the infrastructure layer (e.g., Layer 1s), dApps should prioritize usability over technological merit. This overemphasis on technical sophistication may explain why there are only a few truly effective dApps in the ecosystem.

For the consumer dApp space to advance we should start shifting from 1 to 2.

A+ Developers → Fully Developed dApp → Attention

Minimum Viable dApp (built by anyone) → Attention → A+ Developers

The most successful dApps, from Aave to Pump.fun, tend to follow the second path. For example, Uniswap's founder, Hayden Adams, had coding experience before building Uniswap.

I believe the dApp development process will evolve from "build it and they will come" to "iterate until they come, then go deep." The rapid growth of the Solana memecoin ecosystem illustrates this, with launchpads, smart contract auditors (e.g., RugCheck), trading bots, and more emerging quickly. Where there’s attention, there’s opportunity.

In this co-creative environment, we should optimize for:

Empowering Users to Become Builders – Develop tools like no-code generative AI platforms trained on blockchain SDKs to enable anyone to ideate and build. A GPT Store-like interface, combined with financial incentives for dApp creators, can effectively convert users and traders into builders.

Facilitating Liquidity and Low Gas Fees – Affordable dApp deployment encourages users to experiment and vote with their wallets.

Establishing Smart Contract Safety Standards – To create a safe development environment, implement safer programming languages (e.g., Move), real-time AI-driven contract safety tools, and bug bounty marketplaces.

Implementing Thoughtful Tokenomics – Consider tokenomics experiments that allow the foundation to take a small fee from each app's revenue (especially those built with foundation-provided generative AI tools) or a percentage of tokens. This ensures that value flows back to the base chain treasury, avoiding pitfalls like those experienced with Pump.fun.

Financial Gains Are the Ultimate Onboarding Tool

When onboarding the next billion users, financial incentives matter for both retail and institutional participants. Before dismissing memecoins in favor of attracting "real" users, we must acknowledge that memecoins have drawn more retail participants on-chain than any other use case. The financial allure of NFTs has similarly attracted collectors and artists; only those achieving financial success or motivated by non-monetary factors have remained.

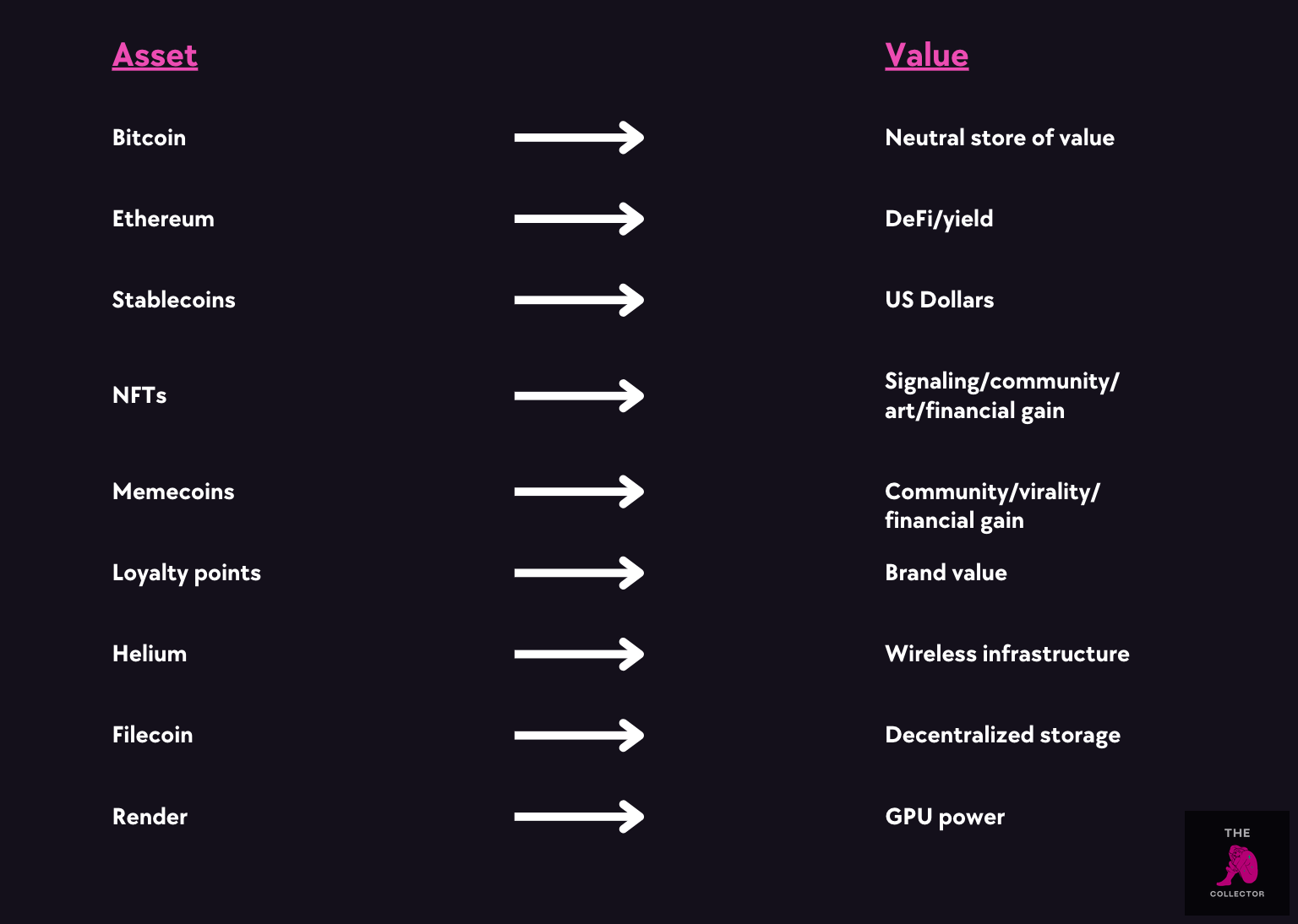

Currently, financial gain is the primary use case in crypto, manifesting through yield generation and meme coin trading. The sustainability of this trend hinges on the desirability of the underlying value. At its core, crypto's fundamental use case revolves around holding, trading, and transferring value—whether that be Bitcoin, stablecoins, memecoins, loyalty points, or reputation scores.

For an asset to hold significance, its underlying value must resonate both financially and socially. A token's market capitalization reflects its importance by discounting project execution risk while incorporating narrative premiums (effectively forecasting its future relevance).

Stablecoins have found product-market fit largely because the US dollar serves as a trusted store of value, thanks to its historical stability.

The users = builders framework extends to enterprises as well, but we must consider additional factors:

Value Capture: How effectively can the company capture value?

Risk Aversion: What is the company’s level of risk tolerance?

Legacy Integration: How seamlessly can it integrate with existing systems?

Enterprises prioritize stability over performance, often re-examining their performance only when stability is threatened. The direct competition from crypto’s seamless peer-to-peer stablecoin payments has forced fintechs like PayPal and Stripe to adopt this technology rapidly.

Expect to see similar shifts across various industries:

Bitcoin's outperformance relative to other asset classes has accelerated ETF adoption. As Solana continues to excel, its chances of securing an ETF will increase.

Streamlined blockchain settlement processes will prompt banks to integrate blockchain technology into their infrastructure.

The underperformance of private equity will drive the search for alternative yield sources and expand the range of alternative assets available to retail investors. This will also lead to the emergence of private equity funds leveraging Web3 technology to drive growth.

Financial gains are also essential for advancing the ecosystem, whether through Ethereum’s treasury supporting the Ethereum Foundation or altcoin projects that elevate their most successful traders to full-time ambassador roles.

Competition for APAC Users and Developers Is Intense

The new Layer 1s are actively incorporating APAC into their strategies through ecosystem funding for developers, hackathons, community groups, and recruitment efforts. Several factors drive this focus:

The region boasts a significant number of crypto-native users, as indicated by the popularity of Axie Infinity in 2021 and OpenSocial today

APAC ranks as the fifth-largest region for developers, although growth is not as rapid as in other areas

Source: a16z

Countries like Japan and South Korea provide improved regulatory clarity, fostering a more conducive environment for blockchain development

The region features a young, tech-savvy consumer base accustomed to online value transfer through popular apps like Lazada, Tokopedia, GoTo, Rakuten, and Kakao

New Layer 1s Are Fighting Against Time

Monolithic Layer 1s vs. Modular Ethereum Layer 2s

Ethereum faces urgent pressure to develop a high-performance, unified Layer 2 ecosystem. Multiple innovative teams (e.g., MegaETH, Odyssey, Uniswap, Fuel) are working on scalability solutions, alongside culture-led Layer 2s like Abstract and ApeChain. Additionally, Ethereum Layer 2s facilitate the distribution of sequencer revenues, such as Shape L2 distributing 80% of sequencer fees to artists and applications.

Meanwhile, monolithic Layer 1s like Solana are gaining traction in practical applications, despite Ethereum's dominance in total value locked (TVL) and stablecoin volume. Notable shifts, like Sky (formerly Maker) moving to Solana, signal a changing landscape, with Decentralized Physical Infrastructure (DePIN) emerging as a leading use case.

New Layer 1s vs. Solana

Solana's upcoming Firedancer implementation promises theoretical throughput of 1 million transactions per second (TPS), increasing pressure on competitors like Sui. However, Solana must retain existing dApps, prevent migration to other high-performance Layer 1s, and successfully implement promised performance enhancements.

Mainnet Layer 1s vs. Pre-Mainnet Layer 1s

Pre-mainnet Layer 1s, such as Berachain and Monad, face a three-fold challenge:

Competing with Solana's performance improvements

Competing with Ethereum's evolving ecosystem

Building brand recognition against established alternative Layer 1s

Generalized vs. Specialized Layer 1s

While general-purpose Layer 1s were once all the rage, we are increasingly seeing specialized Layer 1s, such as:

Hyperliquid — Perpetual DEX L1

Story Protocol – The Intellectual Property L1

Vana – The data ownership L1

For instance, Hyperliquid, the perpetual DEX Layer 1, has a similar Total Value Locked (TVL) to Aptos and Sei while exceeding that of Sei.

These specialized chains provide:

Greater autonomy

Higher funding round potential

Tailored tech stacks and architectures

Story Protocol — Proof of Creativity consensus mechanism

Vana — Nagoya Consensus

Hyperliquid — HyperBFT consensus mechanism

This creates a complex web of technological and adoption races in the Layer 1 space, where timing and execution are critical for success.

Concluding Remarks

The Layer 1 landscape has moved past the era of competing purely on performance metrics into a complex interplay of community, culture, and practical utility. While each new L1 brings innovations - from Sui's gaming architecture to Berachain's proof-of-liquidity mechanism - Solana's established ecosystem and cultural momentum present a formidable moat that mere technical improvements cannot easily overcome.

The emerging L1s demonstrate two distinct attempts toward market relevance:

The community-first approach of Monad and Berachain, building cultural resonance and user engagement before launch

The institutional strategy of Aptos and Sei, pursuing enterprise adoption and traditional finance integration

These new L1s face urgent pressure from multiple directions: Solana's continuous technical improvements, Ethereum's evolving L2 ecosystem, and competition for developer mindshare. Additionally, the fierce battle for APAC market dominance and the critical role of financial incentives in driving user adoption create a complex competitive landscape that demands swift, strategic execution.

Solana's success stems from striking an effective balance: maintaining "good enough" technology that continuously improves while fostering a thriving ecosystem of practical applications, particularly in DePIN and consumer products. This combination of technical adequacy and genuine utility has created network effects that new L1s must thoughtfully approach.

Early evidence suggests specialized optimization may offer one viable path forward. The emergence of focused L1s like Hyperliquid for perpetual DEXs, Story Protocol for IP management, and Vana for data ownership points to increased experimentation with purpose-built chains. These specialized platforms can offer:

Architectural designs optimized for specific use cases

Greater autonomy in governance and development

Focused community building around clear value propositions

Targeted developer experiences and incentives

While it's too early to determine which strategies will ultimately succeed, current market dynamics suggest two potential approaches:

Establishing strong positions in specific market niches rather than attempting to replicate Solana's general-purpose success

Creating complementary ecosystems that enhance rather than replace existing blockchain infrastructure

In the end, survival in the L1 space won't come from just technical superiority over Solana—it will come from finding distinct markets, building devoted communities, and using financial incentives to drive sustained adoption.

I'm looking to collaborate with an investment fund focused on identifying the future of this space. If you're part of one, feel free to reach out.

Additionally, if you’re seeking Web3 app ideas or building a business in Web3 and need advice or customer research, don’t hesitate to get in touch.

Contact: enquiries@nakedcollector.xyz

This is incredibly in-depth! Thanks for the article ser