AI Agents: How to Position for the $100B+ Opportunity

Join industry giants like Coinbase, McKinsey, HBS, Coinbase, JPM and leading VCs for unparalleled independent insights. Subscribe now and stay ahead of the curve.

🔔 Quick Updates:

Just dropped a deep dive on RTFKT with Pet Berisha - definitely check it out if you haven't already! It's a fascinating look at their evolution through the years.

💼 Career Update:

After seven years in crypto, I'm looking to dive deeper into the VC/hedge fund side of things. If you're at (or know folks at) crypto-native funds, I'd love to connect! Reach out on Twitter or shoot me an email.

Now, let's dive into today's analysis...

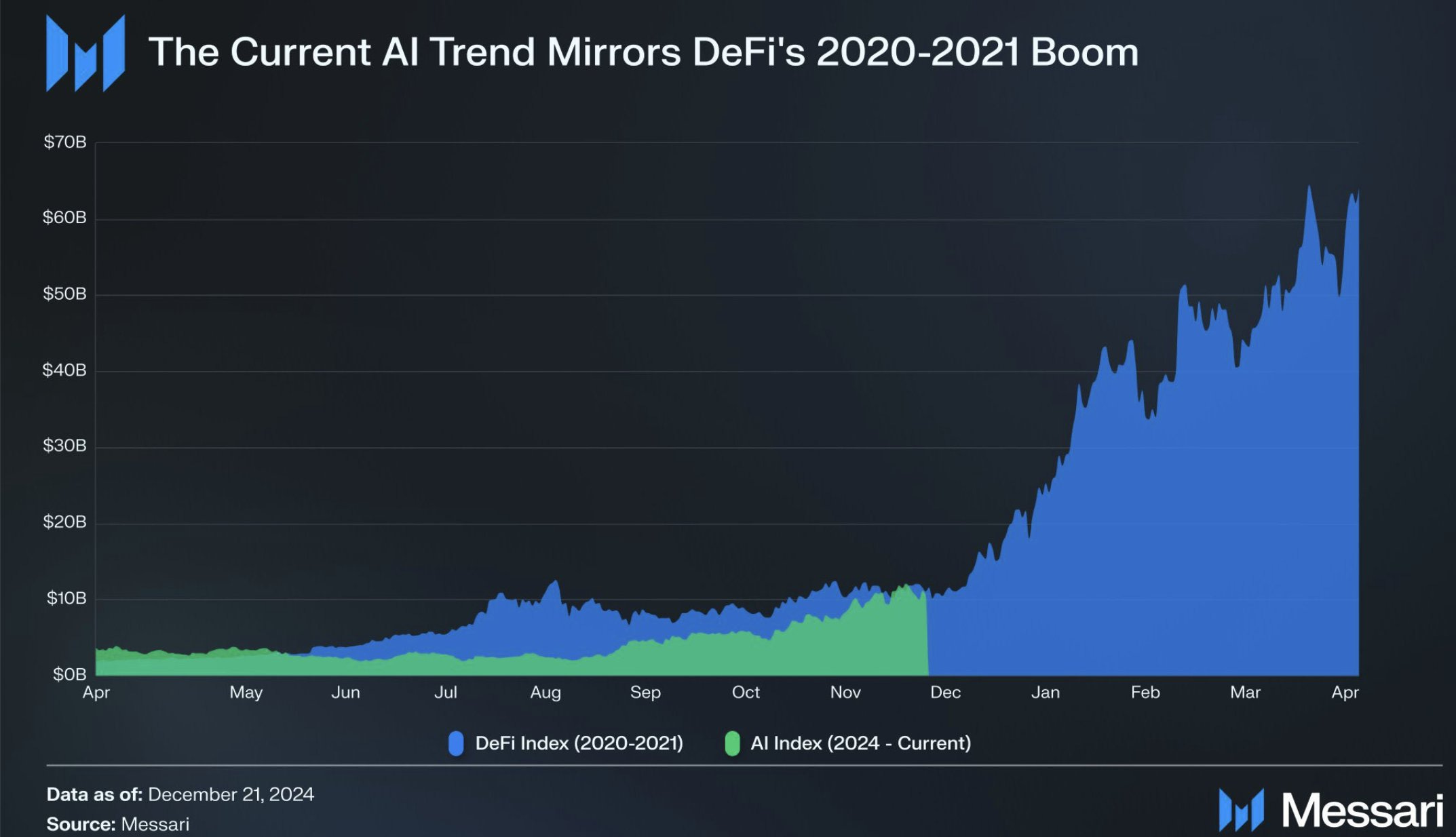

While the recent price slowdown in AI cryptocurrencies has sparked debate about the longevity of AI Agent projects, signs point to transformative innovations ahead, similar to DeFi's emergence in 2020. By now, you’ve all probably seen the chart below.

However, with new tokens launching daily, investors face a critical question: which segments of the AI Agents space offer the strongest upside potential?

Having analyzed the convergence of AI and crypto since correctly predicting AI companions and on-chain AI models in late 2022, I've observed how these early concepts are now materializing in DeFAI (AI x Decentralized Finance). The AI Wayfinder whitepaper in early 2024 first highlighted DeFAI's potential to dominate the intersection of crypto and AI. However, understanding the sector's potential requires a deeper structural analysis.

Here's a comprehensive framework for evaluating the entire AI Agent ecosystem:

The 5 AI Agent categories:

The App

The App Store

The Fund

The Framework

Infrastructure

1. The App

We've seen multiple 10x+ gains from agents like AIXBT to most recently Fresya AI which has done a 2.5x in January alone. This category is the most customer-facing.

Valuation Cap:

Optimistic: Anywhere from $1B+ (Mr. Beast valuation) for entertainment agents to $22.5B (Bloomberg terminal valuation in 2023) for utility with proprietary terminals like AIXBT.

Just like with the Bloomberg Terminal, the barriers to accessing the best AI Agent terminals remain high (AIXBT's terminal access costs ~$300,000). This is key to preserve exclusivity and avoid leaking too much alpha. As a consequence, for regular token holders, this means zero fundamental utility - the token serves purely as a speculation vehicle on agent adoption. Applications for the terminals could extend beyond crypto to sports betting, traditional markets, and business intelligence.

Realistic: $96.4M

Assumptions

Revenue = $5,200,000/year (Assuming Ivan on Tech's, one of the highest paid crypto influencers, pricing at 1x review per week.

Advertising/Marketing Services Average EV/Revenue (as of January 2025) = 18.53

Pros:

Natural marketing pipeline — agents like AIXBT automatically market their own token through content, creating a flywheel of attention. Thus, marketing cost is effectively = zero (only pay for the cost of inference). Tokenization is also one of the few ways creators and experts can earn from their expertise in the AI landscape.

Cons:

Web2 companies like OpenAI and X could easily render some of these agents valueless via new updates. E.g. what if Grok learns to scan Twitter timeline better than AIXBT? Also, platforms like Cookie or Kaito could "democratize" access to alpha making alpha agents less necessary. AI Agents (Web2 and Web3) still have memory constraints. Higher cost of inference for more advanced models (if using APIs), high cost of training if train your own model. Cost of inference for each query – access to agent has to be limited otherwise costs could exceed revenues. Dependency on OpenAI, Anthropic APIs.

What to Look For:

Unique training data, good/unique data pipelines, developers with quantitative/trading backgrounds.

Ease of Discovery:

Medium. While AI Agents are easy to assess on the entertainment front, the alpha/investment advice is harder. For instance, some believe that AIXBT is pure alpha when in fact some of its tweets have been hallucinations if you look deeper into them. Requires backtesting and verify validity of tweets.

Revenue Model:

Fees for 1-to-1 attention.

Examples:

$AIXBT, $MOBY, $SCOUT, $DKING, $ANON, $1000x

(Not investment advice.)

Investment Score:

8/10

2. The App Store

The App Store concept is wide and is among the highest potential categories. Encompasses a vast array of platforms from AI Agent launchpads to AI gaming. Differs from AI Agents by providing a two-sided marketplace (not just protocol to user, but also user to protocol). Differs from The Framework by relying on some level of closed-source technology. Often takes longer time to build than other categories.

Valuation Cap:

Optimistic: $280B

Assumptions: $30B Apple App Store 2024 revenue * Apple's 9.26EV/R ratio

Realistic: $2.7B – $14B

Character.ai (an AI character “app store”) acquired by Google for $2.7B

Uniswap’s FDV is $14B

Pros:

Power law applies. Top platform could reach a very high market cap. Launchpads and DEXes have some of the highest revenues in crypto after stablecoins. Closed source elements create moats.

Cons:

Due to the open nature of crypto tokens can be traded anywhere. The platform with the best LP mechanism (thus lower fees) will gather liquidity. This means competitive edge may not lie in the “AI tech” but in LP and tokenomics side, making it closer to a DEX not an AI play. For instance,

The AI Agent AIXBT, with its proprietary framework, could've launched anywhere but chose Virtuals due to the attention Virtuals had as The App Store for agents. In other words AIXBT didn't utilize Virtuals “AI tech” itself due to its limited nature. Same thing occurred when the 1000xPod agent launched on Virtuals but used the Eliza framework as its tech backbone. It’s safe to say that the best AI Agents are not and will not be built with out of the box tools.

What to Look For:

UI/UX. How easily an advanced agent can be made out of the box, what is the liquidity (how good is the LP mechanism), what is the moat.

The main thing that matters for The App Store is attention. To this end the three competitive levers to pull are 1) first mover advantage (think Pump.Fun), 2) better functionality (think Eliza framework), 3) more value accrual to users via tokenomics (think Blur).

Ease of Discovery:

Medium. Easy to find market leader, but harder to understand tokenomics mean to token holders (e.g. Uniswap and its latent fee switch versus SushiSwap and its great revenue to market cap ratios, during its peak, but poor performance).

Revenue model:

Fees per agent deployment, LP fees, potential partnerships with frameworks (e.g. ability to implement Eliza for a fee).

Examples:

$VIRTUAL, Pump.Fun, DAOS.FUN, $PRIME/$PROMPT, $TOPIA, $GRIFFAIN

(Tokens with a cashtag $ indicate those projects are already tradable or will be in the near future. Not investment advice.)

Investment Score:

9/10. Invest in winners, the best in class.

3. The Fund

Similar concept and value proposition to utility AI Agents, however, biggest difference on the backend and tokenomics side. Instead of sharing alpha publicly it uses it to invest itself. Revenue share or portfolio token airdrops to holders. Future will look like investment DAO with decentralized voting on AI based strategies.

Valuation Cap:

Optimistic: $20B – $40B

Using hedge fund Citadel's AUM*5% (a common valuation practice for hedge funds)

Realistic: ~$4B+

The valuation of OlympusDAO at its peak in 2021

Pros:

Could be seamlessly integrated with Apps (see Section 1) for marketing purposes. Can trade around hype, and outcome not binary. Does not rely on protocols “making it”. Feasible way to democratize fundraising for talented individuals, performance over fundraising.

Cons:

Currently these funds hold a lot of their own token thus making the price movement very reflexive. Currently not yet fully autonomous, human element exists. If autonomous, risk exists that the AI capital allocator goes rogue. Potential of alpha decay (or loss of strategy profitability) with the shifting crypto metas. Faces a lot of competition if uses strictly a launchpad model.

What to Look For:

Does The Fund have systematic alpha other agents and AI fund don't. Does The Fund have interesting proprietary data or data that is hard to access by others (e.g. due to financial constraints or need for experience). Do the tokenomics benefit the holders.

Ease of Discovery:

Medium. Easy to find market leader, but harder to understand tokenomics mean to token holders (e.g. as happened with UNI).

Revenue Model:

Portfolio management fees + % of capital gains

Examples:

(Not investment advice.)

Investment Score:

6/10. Performance benchmarking could take a while so hard to determine good vs. bad funds. Most new funds invest in AI Agents which is a nascent market thus difficult to backtest and hard to identify luck from skill.

4. The Framework

An open-source framework that relies on user/dev flywheel.

Similar to The App Store however focus not just on launching agents but on giving the tools for users to develop more complex ones. Has many similarities with traditional crypto protocols which have open-source code thus rely on building integrations and recognition forward as the competitive edge. Relies on some sort of vertical integration to monetize e.g creator studio or an App Store.

Valuation Cap:

Optimistic: $18B – $700B

$18B = Linux ecosystem value in 2023

$300B – $700B = Using Android’s (semi-open source) economic contribution metrics

Realistic: $6B – $20B

$6B = Aave Protocol’s peak valuation in 2021

$20B = Chainlink’s peak valuation in 2021

Pros:

Can start out small as it could enable a flywheel where studio attracts adoption which attracts developers, which drives integration, which funds development. If framework becomes an important AI module (or Lego as they call them in DeFi) then the protocol could capture a lot of value.

Cons:

May be hard to monetize. Risks of value extractive forks that don't bring back value to the token. Lots of dependencies/ifs. "If devs adopt", "if users adopt". "Build it and they will come" doesn't always work out.

What to Look For:

Developer tech background, Github popularity (stars, forks, commits)

Ease of Discovery:

Hard. Easy to find market leader (Github popularity, market cap), but harder to know if/how the economics will take off.

Revenue Model:

Fees per use e.g. Launch fees, LP fees, usage (dev tools fees). Customer are devs.

Examples:

(Not investment advice.)

Investment Score:

8/10. Hard to know if network effects have been achieved, but if they have, this could be the category with the most potential.

5. The Infrastructure Provider

Essentially a cog in the machine, the more important it is the higher valuation it could get. Could be a better data source or improved agent memory.

Valuation Cap:

Optimistic: $22.5B – $27B

$22.5B = Bloomberg terminal valuation in 2023)

$27B = Refinitiv’s valuation in 2019

Realistic: $135M – $20B

$135M= Blockworks valuation

$750M = Nansen Valuation Leading

$20B = Chainlink’s peak valuation in 2021

Pros:

Proven business model with potential for good consistent revenue. Likely targets for M&A.

Cons:

A lot of competition: Nansen, Kaito, Cookie, Dune, Flipside are all working on providing users with alpha. However, sources of alpha change constantly.

What to Look For:

User experience and usefulness of data. Quality of unique data.

Ease of Discovery:

Easy. Crypto Twitter discussions are a good indicator.

Revenue Model:

Fees to access, ad revenue

Example:

$COOKIE, Kaito AI, $ACOLYT, $GRPH

(Tokens with a cashtag $ indicate those projects are already tradable or will be in the near future. Not investment advice.)

Investment Score:

6/10. Most good projects in this category have usually been reserved for VCs but the Hype Protocol, Cookie.Fun and the Kaito AI Yaps examples could lead to more democratized opportunities.

Conclusion

A good way to think of the AI Agent space is by replacing "DeFi Legos" with "AI Legos". An AI Agent could be launched on Virtuals, interface could be ai16z, data backend could be Acolyte, memory could be augmented by Soulgraph.

AI Agents will start having modular (multiple component build) vs. monolithic (all-in-one frameworks) design discussions.

While Web3 agents have crypto-native integration advantage over their Web2 counterparts, it’s still unclear what long-term moats they may have.

The ultimate goal for projects in the AI Agent space is to create an ecosystem of Apps, App Stores, Framework and Infrastructure.

Value will be captured by 1) being the best in class of that category e.g. the Chainlink or Aave of AI and/or, 2) building the best vertical stack/ecosystem.

Being close to consumer is important in this cycle (The Agent and The App Store are the closest to the consumer).

The Frameworks could be considered as the new "Layer 1s". Just like the current Layer 1s obfuscated things like hardware and energy demands from the user, these new "Layer 1s" will obfuscate the blockchain demands from the user.

While it's hard to predict which protocols will be most valuable the same things that matter for protocol valuations today will matter in this new AI context as well:

How well the tokenomics capture value to the holders – Fees and revenue share are good indicators

Is there narrative/hype around it — Public/news discussion around LLMs (NVIDIA, OpenAI and DeepSeek) is a good proxy

Protocol's replaceability in the AI hierarchy – Is the protocol the Uniswap of DEXes or the Chainlink of oracles?

Developer tooling – How easy it is to create new advanced use-cases

Although some have said that AI Agents don't have as strong network effects as DeFi, I disagree. I believe the platform with the most use-specific training data in their segment will win. E.g. there will be no point in using the second-best AI on-chain trader.

Hence, while it's still way too early to declare winners, the power law applies especially strongly to the AI category:

More users → more training data → better outputs → more users

Given these considerations, the three most important questions you can ask yourself are:

Are there network effects?

Is there an ecosystem forming around the token?

Does having the token make sense (e.g. revenue share, buyback and burn, token gating, etc.)